What is an FHA Purchase Loan? If you are looking to buy a home in…

Your Ultimate Guide to a First-Time Homebuyer Mortgage in Houston

Navigating First-Time Buyer Loans in Texas

Buying your first home in Houston is an exciting milestone, but finding the right first time homebuyer mortgage can feel overwhelming. At Your Texas Home Loan Guy, we specialize in helping Texans unlock the doors to their dream properties with tailored financing solutions.

As experts in the local market, we know that every buyer’s financial situation is unique. Whether you are exploring a traditional FHA purchase loan or looking into local down payment assistance programs, our goal is to provide clear, educational guidance. In fact, we are experts at providing second opinions on first-time homebuyer mortgages. If you already have a quote from another lender, let Jimmy Rushing review it to ensure you are getting the best possible terms for your First-Time Buyer Loans.

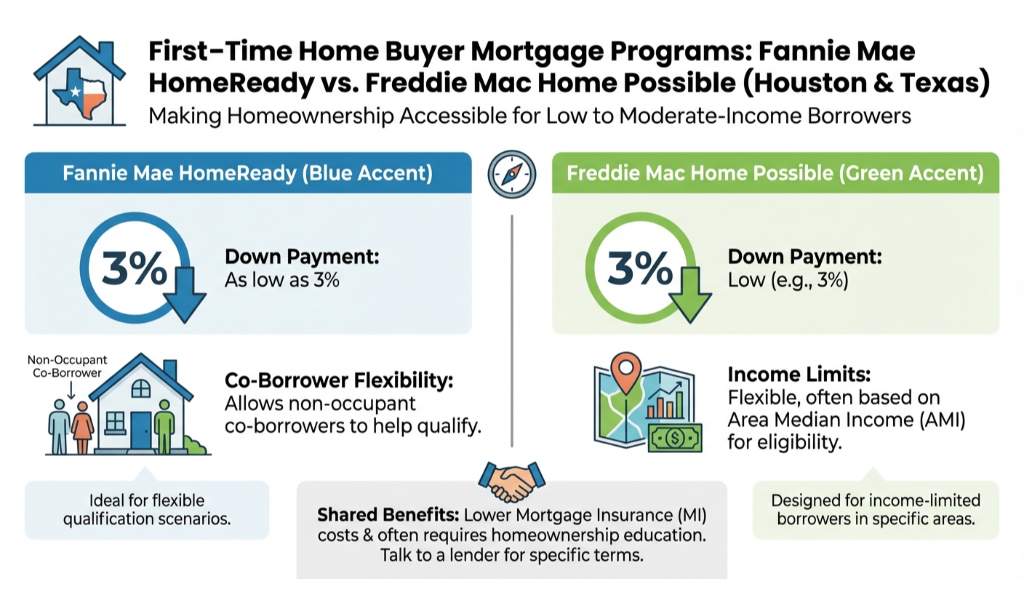

Top First-Time Home Buyer Mortgage Options: HomeReady and Home Possible

When it comes to securing a First-Time Home Buyer Mortgage, two of the most popular conventional loan programs are Fannie Mae’s HomeReady and Freddie Mac’s Home Possible. Both programs are designed to make homeownership more accessible for low to moderate-income borrowers in Houston and across Texas.

- Fannie Mae HomeReady: This program allows for a down payment as low as 3 percent. It is highly flexible, allowing co-borrowers who do not live in the home to help you qualify.

- Freddie Mac Home Possible: Similar to HomeReady, this option also requires just a 3 percent down payment. It offers reduced mortgage insurance premiums, which can significantly lower your monthly payments.

Choosing between these two first-time homebuyer mortgage programs depends on your specific credit profile and income level. Our team can evaluate your financial scenario and guide you toward the program that best fits your Texas homeownership goals.

| Program Feature | Fannie Mae HomeReady | Freddie Mac Home Possible |

|---|---|---|

| Minimum Down Payment | 3% | 3% |

| Minimum Credit Score | Typically 620 | Typically 660 |

| Income Limits | Up to 80% of Area Median Income (AMI) | Up to 80% of Area Median Income (AMI) |

| Non-Occupant Co-Borrowers | Allowed | Not Allowed |

Why Get a Second Opinion on Your Mortgage?

Many buyers accept the very first loan offer they receive, potentially leaving thousands of dollars on the table over the life of the loan. Because we are experts at providing second opinions on first-time homebuyer mortgages, we highly recommend letting us review your initial pre-approval. We will analyze the interest rate, closing costs, and overall loan structure.

Working with a dedicated Houston mortgage broker like Jimmy Rushing ensures you have an advocate in your corner. We pride ourselves on excellent communication, easy accessibility, and a commitment to helping you build wealth through real estate. Do not settle for a one-size-fits-all approach when applying for First-Time Buyer Loans. Let us customize a solution that works perfectly for your budget.

Q1: What qualifies someone for a first time homebuyer mortgage in Texas?

Generally, you are considered a first-time homebuyer if you have not owned a principal residence in the past three years. This status opens up access to various specialized loan programs and lower down payment options.

Q2: Can I buy a home in Houston with no down payment?

Yes, certain programs like VA loans or USDA loans offer zero down payment options for eligible borrowers. Additionally, pairing a conventional or FHA loan with down payment assistance programs can significantly reduce your upfront costs.

Q3: How does a HomeReady loan differ from an FHA loan?

While both are great for first-time buyers, HomeReady is a conventional loan that allows you to cancel mortgage insurance once you reach 20 percent equity. FHA loans require mortgage insurance for the life of the loan if you put down less than 10 percent.

Q4: Why should I get a second opinion on my mortgage offer?

Different lenders have different rates, fees, and loan products. We are experts at providing second opinions on first-time homebuyer mortgages and can often find lower rates or better loan structures that save you money.

Q5: What is the minimum credit score needed for First-Time Buyer Loans?

Credit score requirements vary by program. FHA loans can accept scores as low as 580 for a 3.5 percent down payment, while conventional programs like Home Possible typically require a score of 620 or higher.

Ready to explore your first-time homebuyer mortgage options in Houston? Contact Jimmy Rushing today!

Related Posts