Why Choose a 15-Year Fixed Mortgage for Your Texas Home? When you are looking to…

The Ultimate Guide to an Assumable Mortgage in Houston, TX

What is an Assumable Mortgage and How Does Mortgage Assumption Work?

If you are looking to buy a home in Houston, TX, you might have heard the term assumable mortgage. Also known as a mortgage assumption, this unique financing option allows a buyer to take over the seller’s current mortgage terms, including their interest rate, repayment period, and current principal balance. In a market where interest rates fluctuate, taking over a historically low rate can save you thousands of dollars over the life of the loan.

Not all home loans qualify for this process. Generally, conventional loans are not assumable. However, government-backed loans usually are. At Your Texas Home Loan Guy, we specialize in guiding Houston homebuyers through these complex transactions. If you have been told you do not qualify or if you are facing hurdles, we are experts at providing second opinions on assumable mortgages.

To help you navigate your options, it is important to understand the specific rules for the three main types of government-backed assumable loans:

- FHA Assumable Loans: Perfect for many first-time buyers. You can learn more about standard FHA options on our FHA purchase loan page.

- VA Assumable Loans: A great benefit for veterans and active-duty military. Check out our VA purchase loan guide for more details.

- USDA Assumable Loans: Designed for rural and suburban homebuyers who meet specific income limits.

Comparing FHA, VA, and USDA Assumable Loans

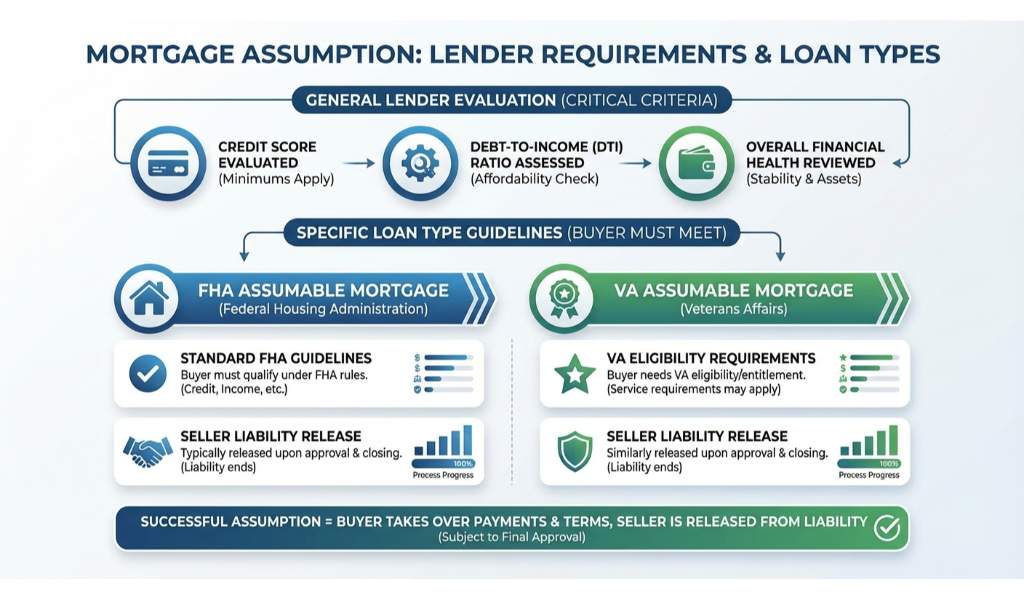

When considering a mortgage assumption, you must meet the specific lender requirements for the loan type you are taking over. The lender will evaluate your credit score, debt-to-income ratio, and overall financial health to ensure you can afford the monthly payments.

For an FHA assumable mortgage, the buyer must meet standard Federal Housing Administration guidelines. The seller is typically released from liability once the assumption is approved and closed. Similarly, a VA assumable mortgage allows buyers to take over the loan of a veteran. Interestingly, the buyer does not strictly have to be a veteran themselves, but if they are not, the original veteran seller’s VA entitlement remains tied up in the property until the loan is paid off. A USDA assumable mortgage requires the buyer to meet the USDA strict income and property location guidelines.

One major consideration with an assumable mortgage is the equity gap. If the seller has a lot of equity, you will need to cover the difference between the home purchase price and the remaining loan balance. You can do this with cash or a second mortgage. If an assumption does not work out for your situation, you might also explore a rate and term refinance down the road to secure better terms on a traditional loan.

| Loan Type | Assumability Status | Key Requirement | Seller Liability Release |

|---|---|---|---|

| FHA Loan | Highly Assumable | Buyer must meet FHA credit and income standards | Yes, upon lender approval |

| VA Loan | Highly Assumable | Buyer must pay a VA funding fee (usually 0.5%) | Yes, but VA entitlement may remain tied up |

| USDA Loan | Assumable | Property must be in an eligible rural area | Yes, upon lender approval |

| Conventional Loan | Rarely Assumable | Usually contains a ‘Due on Sale’ clause | Not Applicable |

Why Choose Jimmy Rushing for Your Houston Mortgage Needs?

Navigating the real estate market in Houston, TX, requires a knowledgeable local expert. Jimmy Rushing, your dedicated mortgage broker, understands the nuances of the local market and the complexities of mortgage assumption. The process of assuming a loan can be lengthy and requires meticulous paperwork. Lenders are notoriously slow with assumptions because they do not make as much money on them compared to originating a new loan.

This is where having an experienced advocate makes a massive difference. We are experts at providing second opinions on assumable mortgages. If another lender has denied your assumption application or given you confusing information, let us review your file. We will give you honest, straightforward advice on whether an assumable mortgage is truly your best path forward, or if alternative financing options would serve you better.

Q1: What is an assumable mortgage?

An assumable mortgage allows a homebuyer to take over the seller’s existing loan terms, including the interest rate, remaining balance, and repayment schedule.

Q2: Are all mortgages assumable in Texas?

No. Most conventional loans are not assumable. Typically, only government-backed loans like FHA, VA, and USDA loans allow for a mortgage assumption.

Q3: How do I cover the equity gap in an assumable mortgage?

If the home price is higher than the remaining mortgage balance, the buyer must cover the difference. This can be done using a cash down payment or by securing a second mortgage.

Q4: Do I need good credit to assume a mortgage?

Yes. The lender must approve you for the assumption, which means you must meet their specific credit score, income, and debt-to-income ratio requirements.

Q5: Can I get a second opinion if my mortgage assumption is denied?

Absolutely. Jimmy Rushing and the team at Your Texas Home Loan Guy are experts at providing second opinions on assumable mortgages and can help you explore all available financing options.

Related Posts