Understanding the Cash-Out Mortgage: Is It Right for You? If you are a homeowner in…

Your Guide to Houston Condo Mortgage Financing and Loans

Understanding Condo Loans: Warrantable vs. Non-Warrantable Condos

If you are looking to purchase a condominium in Houston, TX, navigating the world of condo mortgage financing can feel a bit different than buying a single-family home. At Your Texas Home Loan Guy, we specialize in helping buyers secure the right condo loans for their unique needs. The most critical factor in condo financing is whether the property is considered warrantable or non-warrantable.

- Warrantable Condos: These properties meet the strict guidelines set by Fannie Mae and Freddie Mac. They are typically easier to finance and often qualify for a standard conventional fixed rate mortgage.

- Non-Warrantable Condos: These do not meet standard agency guidelines, often because a single entity owns too many units, or the homeowners association (HOA) is involved in litigation. Financing these requires specialized portfolio lenders.

As local Houston mortgage brokers, we are experts at providing second opinions on condo financing. If you have been turned down elsewhere due to HOA issues, let us take a look.

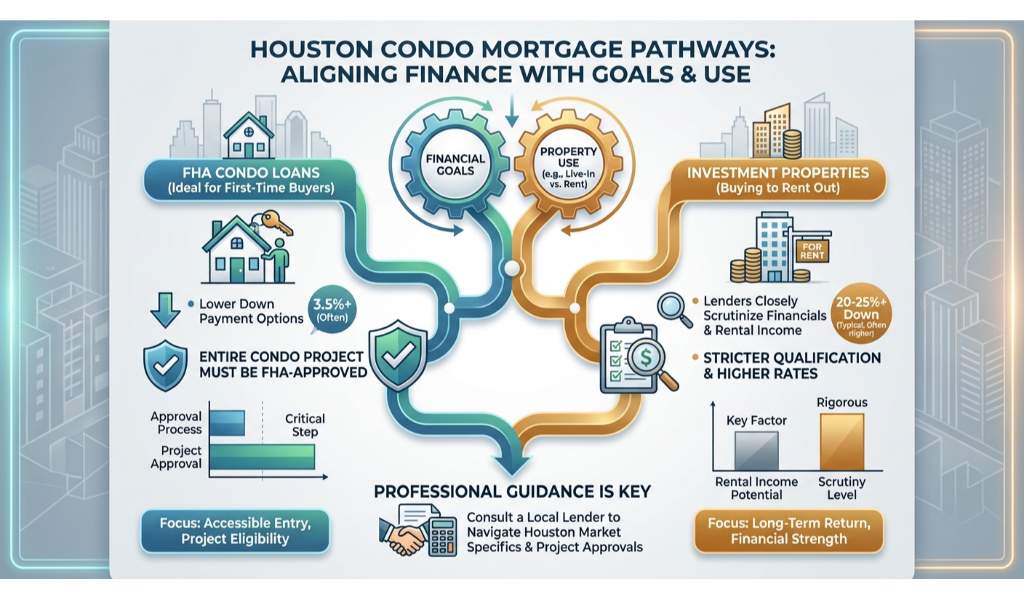

Exploring Your Condo Financing Options

Securing the right mortgage for your new Houston condo depends heavily on your financial goals and how you plan to use the property. There are several pathways for condo mortgage financing:

- FHA Condo Loans: Ideal for first-time buyers, an FHA purchase loan offers lower down payment options. However, the entire condo project must be FHA-approved.

- Investment Properties: Buying a condo to rent out? You will want to explore an investment property mortgage. Keep in mind that lenders closely scrutinize the ratio of owner-occupied units versus rentals in the building.

Jimmy Rushing and the team at Your Texas Home Loan Guy know the Houston market inside and out. We help you navigate the complex HOA questionnaires and secure the best possible rates for your condo loans.

| Loan Type | Minimum Down Payment | Condo Approval Required? | Best For |

|---|---|---|---|

| Conventional (Warrantable) | 3% to 5% | Yes (Limited or Full Review) | Primary residences with strong credit |

| FHA Loan | 3.5% | Yes (HUD Approved List) | First-time buyers needing flexible credit |

| Non-Warrantable Portfolio | 10% to 20% | Lender Specific | Condos with HOA litigation or high investor ratios |

| Investment Property | 15% to 25% | Yes (Full Review) | Real estate investors generating rental income |

Why Get a Second Opinion on Your Condo Mortgage?

Condo mortgage financing can be tricky. Many buyers are told their dream condo is un-financeable simply because their current lender does not have access to the right loan products. That is exactly why we are experts at providing second opinions on condo financing.

Before you give up on that perfect Houston high-rise or cozy suburban townhouse, let Jimmy Rushing review your scenario. We have access to a wide network of wholesale lenders, allowing us to find creative solutions for both warrantable and non-warrantable properties. Your Texas Home Loan Guy is dedicated to making your condo ownership dreams a reality with transparent, competitive condo loans.

Q1: What is the difference between a warrantable and non-warrantable condo?

A warrantable condo meets the lending requirements of government-backed entities like Fannie Mae and Freddie Mac. A non-warrantable condo does not, usually due to issues like pending HOA litigation or a high concentration of investor-owned units.

Q2: Can I get an FHA loan for a condo in Houston?

Yes, you can secure an FHA loan for a condo, provided the entire condominium complex is on the HUD-approved list. If it is not, the HOA may need to apply for approval.

Q3: Do condo loans have higher interest rates than single-family homes?

Sometimes. Lenders often apply a small pricing adjustment for condo loans because they carry slightly more risk due to the shared structural and financial responsibilities of the HOA.

Q4: Why do lenders care about the condo HOA?

The financial health of the HOA directly impacts the value and safety of the property. Lenders review HOA budgets and insurance policies to ensure the building is properly maintained and financially stable.

Q5: What should I do if my condo loan is denied?

Do not panic. We are experts at providing second opinions on condo financing. Reach out to Your Texas Home Loan Guy, and we can explore portfolio loans and other specialized options that your previous lender may not have offered.

Call Jimmy Rushing at (713) 822-6347 for Your Condo Loan Second Opinion

Related Posts