The Shift from High-Pressure Sales to Empowered Homeownership in Houston When you are preparing to…

First-Time Homebuyers in Houston: Creative Paths to Ownership When Prices Feel Out of Reach

Navigating the Houston Housing Market as a First-Time Buyer

Houston is a vibrant, rapidly growing city, but for many first-time homebuyers, the current real estate market can feel a bit overwhelming. With rising property values and shifting interest rates, securing your dream home might seem out of reach. However, achieving homeownership in Houston is entirely possible when you have the right strategies and a knowledgeable local expert in your corner.

As Jimmy Rushing, your dedicated Houston mortgage broker, I am here to help you discover creative paths to homeownership. At Your TEXAS Home Loan Guy, we specialize in turning complex financial landscapes into clear, actionable steps. Whether you are considering a conventional loan, an FHA loan, a VA loan, or Texas-specific assistance programs, we have the tools to help you build wealth through real estate.

- Conventional Loans: Ideal for buyers with strong credit, offering flexible down payment options.

- FHA Loans: A fantastic choice for first-time buyers needing lower down payments and more forgiving credit requirements.

- VA Loans: A well-deserved benefit for our veterans and active military, offering zero down payment options.

Let us explore how these programs can make buying a home in Houston an exciting reality rather than a stressful challenge.

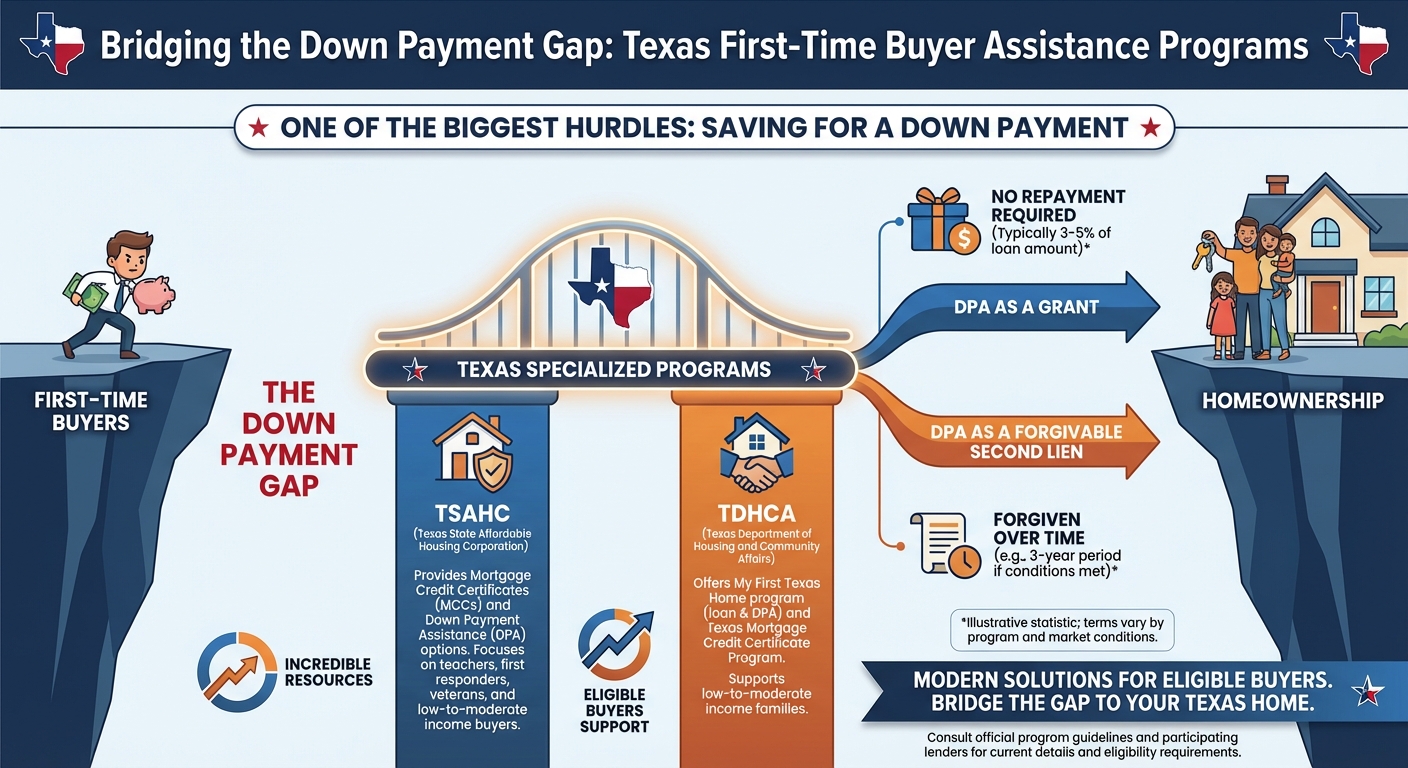

Unlocking Texas-Specific First-Time Homebuyer Programs

One of the biggest hurdles for first-time buyers is saving for a down payment. Fortunately, the great state of Texas offers several specialized programs designed to bridge this gap. Organizations like the Texas State Affordable Housing Corporation (TSAHC) and the Texas Department of Housing and Community Affairs (TDHCA) provide incredible resources for eligible buyers.

These programs often include Down Payment Assistance (DPA), which can be provided as a grant or a forgivable second lien. This means you could receive funds to cover your down payment and closing costs, significantly reducing your out-of-pocket expenses.

- TSAHC Programs: Offers fixed-rate mortgage loans, down payment assistance grants, and mortgage credit certificates for teachers, first responders, veterans, and low-to-moderate-income families.

- TDHCA My First Texas Home: Provides 30-year, fixed-rate mortgages with down payment and closing cost assistance up to 5 percent of the loan amount.

- Mortgage Credit Certificates (MCC): A tax credit that reduces your federal income taxes, freeing up more of your income to qualify for a mortgage.

Working with an experienced Houston mortgage expert ensures you do not miss out on these localized benefits. We carefully evaluate your financial profile to match you with the exact programs that maximize your purchasing power.

| Loan Program | Minimum Down Payment | Typical Minimum Credit Score | Best Suited For |

|---|---|---|---|

| Conventional | 3% (for first-time buyers) | 620 | Buyers with good credit and moderate savings. |

| FHA Loan | 3.5% | 580 | Buyers needing flexible credit and lower down payments. |

| VA Loan | 0% | No strict minimum (lender overlays apply) | Veterans, active-duty military, and eligible spouses. |

| Texas DPA (TSAHC/TDHCA) | Varies (Grants available) | 620 | Low-to-moderate income buyers, teachers, and first responders. |

Preparing for Your Houston Home Purchase

Preparation is the key to success in the competitive Houston real estate market. Before you start touring open houses in Katy, Sugar Land, or The Woodlands, you need a solid financial foundation. The very first step is obtaining a pre-approval. A pre-approval letter not only shows sellers that you are a serious buyer, but it also gives you a clear understanding of your budget.

Here are a few actionable steps to get you closing-ready:

- Review your credit report: Check for any errors and pay down high-interest debt to boost your score.

- Save consistently: Even with down payment assistance, having an emergency fund and earnest money is crucial.

- Gather your documents: Keep your recent pay stubs, W-2s, and bank statements organized and accessible.

At Your TEXAS Home Loan Guy, Jimmy Rushing (NMLS #2520082) and Mpire Financial are committed to educating you throughout this process. We believe that an informed buyer is an empowered buyer. By exploring all available loan scenarios, from FHA to conventional to specialized Texas grants, we tailor a mortgage strategy that fits your unique life goals.

Q1: What is the minimum down payment for a first-time homebuyer in Houston?

First-time buyers can put down as little as 3 percent with certain conventional loans, or 3.5 percent with an FHA loan. Veterans and active military members may even qualify for a zero down payment VA loan.

Q2: Do I have to pay back down payment assistance in Texas?

It depends on the specific program you use. Some down payment assistance comes in the form of a true grant that does not need to be repaid, while others are forgivable second liens that are forgiven after living in the home as your primary residence for a set number of years.

Q3: How do I know if I qualify for a Texas State Affordable Housing Corporation (TSAHC) loan?

Qualification is based on your credit score, total household income, and the county where you plan to purchase the home. Teachers, first responders, and veterans often have access to special TSAHC programs designed specifically for them.

Q4: What is the difference between an FHA loan and a Conventional loan?

FHA loans are government-backed and typically have more lenient credit score requirements, making them great for buyers who are still building credit. Conventional loans are not government-insured and generally require higher credit scores but can offer lower long-term mortgage insurance costs.

Q5: Why should I use a local Houston mortgage broker instead of a big bank?

A local mortgage broker like Jimmy Rushing has access to a wide variety of loan products from multiple wholesale lenders. This means we can shop around to find the best rates and terms for your specific situation, offering a personalized experience and local market expertise that big banks simply cannot match.

Related Posts