Navigating First-Time Buyer Loans in Texas Buying your first home in Houston is an exciting…

Your Complete Guide to a Conventional Fixed-Rate Mortgage in Houston

Understanding the Basics of a Conventional Mortgage

When it comes to buying a home in Houston, Texas, choosing the right financing is a critical step. A conventional mortgage is one of the most popular choices for homebuyers seeking stability and predictable monthly payments. Unlike government-backed loans, a conventional fixed-rate mortgage is offered by private lenders and is not insured by the federal government.

At Your Texas Home Loan Guy, we understand that navigating the Houston real estate market can be complex. Whether you are a first-time buyer or looking to upgrade, securing a 30-year fixed-rate mortgage offers long-term security. If you already have a quote, remember that we are experts at providing second opinions on conventional mortgages to ensure you get the absolute best terms for your financial future.

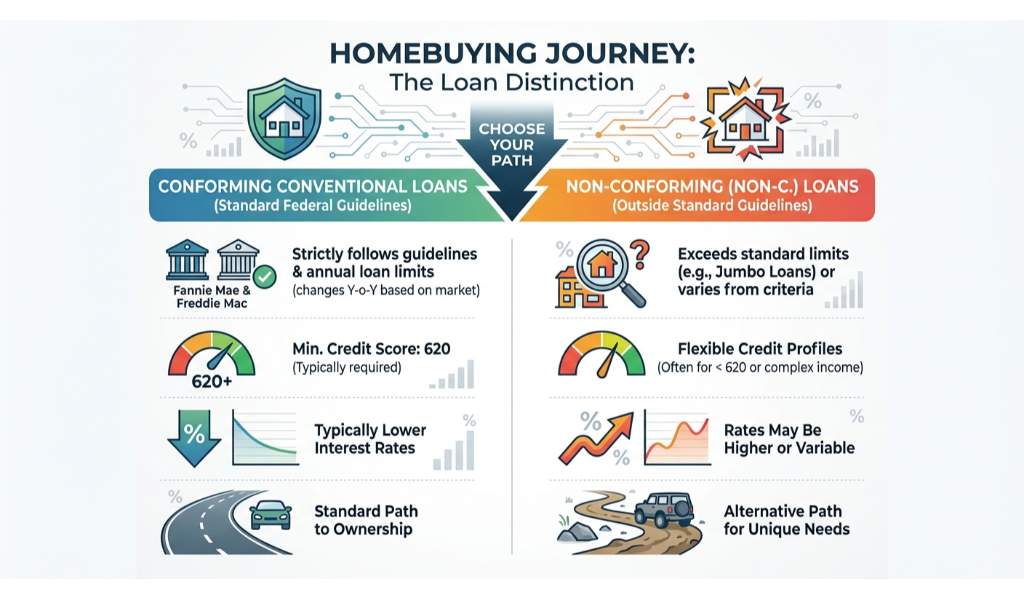

Conforming vs. Non-Conforming Conventional Loans

One of the most important distinctions to understand during your homebuying journey is the difference between conforming and non-conforming loans. A conforming conventional mortgage strictly follows the guidelines set by Fannie Mae and Freddie Mac. This includes specific loan limits that change annually based on the overall housing market.

- Conforming Loans: These mortgages meet standard federal guidelines. They typically offer lower interest rates and require a minimum credit score of 620.

- Non-Conforming Loans: Also known as jumbo loans, these exceed the standard loan limits. If you are eyeing a luxury property in Houston, a jumbo mortgage might be necessary to finance your purchase.

If your credit score or down payment is lower than what a standard conventional loan requires, you might want to explore an FHA purchase loan as an alternative. However, for those with strong credit, a conventional mortgage often yields the most cost-effective long-term results.

| Loan Feature | Conforming Conventional | Non-Conforming (Jumbo) | FHA Loan Alternative |

|---|---|---|---|

| Loan Limits | Within FHFA county limits | Exceeds FHFA limits | Varies by county |

| Minimum Credit Score | Typically 620 | Typically 680 to 700+ | Typically 580 |

| Minimum Down Payment | As low as 3% | 10% to 20% | 3.5% |

| Mortgage Insurance | PMI required if under 20% down | Varies by lender | MIP required for life of loan |

Why Get a Second Opinion on Your Conventional Mortgage?

Securing a home loan is a massive financial commitment. Even a fraction of a percent difference in your interest rate can save or cost you thousands of dollars over the life of your loan. That is exactly why we are experts at providing second opinions on conventional mortgages.

Jimmy Rushing, your trusted Houston mortgage broker, is dedicated to reviewing your current loan estimates. By analyzing your pre-approval, we can often identify better rates, lower fees, or more favorable terms. Do not settle for the first offer you receive. Let us review your conventional fixed-rate mortgage options to give you complete peace of mind.

Q1: What is a conventional fixed-rate mortgage?

A conventional fixed-rate mortgage is a home loan not backed by a government agency, offering an interest rate that remains exactly the same for the entire life of the loan.

Q2: What credit score do I need for a conventional mortgage in Houston?

Most lenders require a minimum credit score of 620 to qualify for a conventional mortgage, though a higher score will help you secure a much better interest rate.

Q3: Are conventional loans better than FHA loans?

It depends heavily on your financial situation. Conventional loans are generally better for buyers with good credit and a larger down payment, while FHA loans are more flexible for buyers with lower credit scores.

Q4: Can I get a second opinion on my mortgage rate?

Absolutely. We highly recommend getting a second opinion. We specialize in reviewing conventional mortgage offers to ensure our clients receive the most competitive terms available in Texas.

Q5: What is the difference between conforming and non-conforming loans?

Conforming loans adhere to the specific loan limits and guidelines set by Fannie Mae and Freddie Mac. Non-conforming loans exceed these limits and are typically used for luxury homes or high-cost real estate markets.

Ready to secure your Houston dream home?

Contact Jimmy Rushing, Your Texas Home Loan Guy, today for expert guidance or a free second opinion on your mortgage offer.

Related Posts