Shifting Your Mindset: Why a Mortgage is a Wealth-Building Tool, Not Just Debt When most…

Your Texas Home Loan Guy’s Top Mortgage Hack: How to Pay Off Your 30-Year Loan Faster Without Refinancing

The Ultimate Houston Mortgage Hack to Save Thousands

Are you staring at a 30-year mortgage and wondering if there is a secret to shaving years off your timeline? You are not alone. As a trusted Houston mortgage broker, I speak with homebuyers every day who want to build wealth faster. The good news is that you do not need a complex financial scheme to make it happen.

Welcome to one of my absolute favorite educational hacks. Jimmy Rushing, Your Texas Home Loan Guy, is here to show you how to beat the system. Many homeowners think the only way to pay off their home loan faster is by refinancing to a 15-year term. While refinancing is a powerful tool, it is not the only option. In fact, you can achieve massive interest savings without paying a single dime in closing costs.

- Keep your current low interest rate.

- Avoid the fees associated with a new loan.

- Maintain flexibility in your monthly budget.

How the Extra Payment Strategy Works

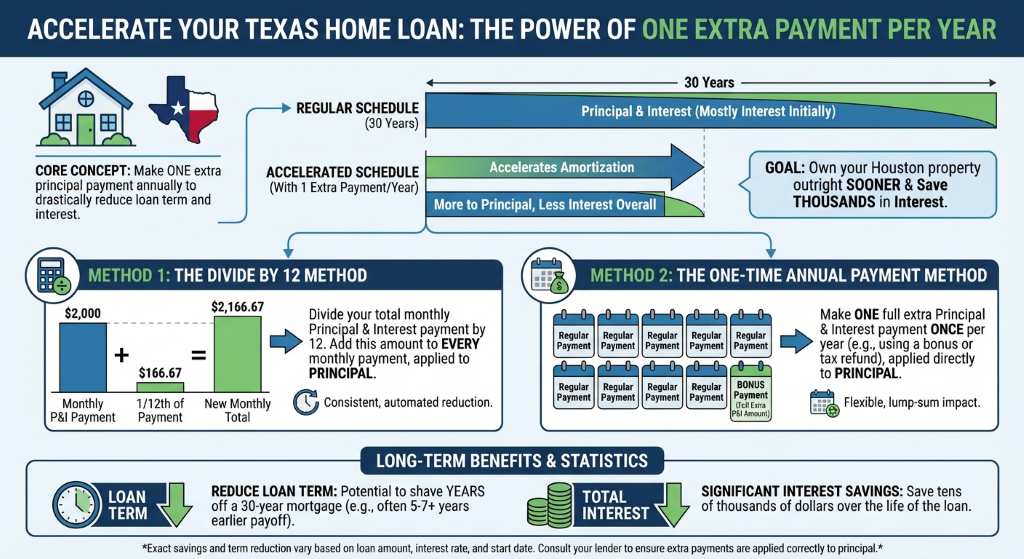

The core of this Texas home loan hack is surprisingly simple. By making just one extra mortgage payment per year applied directly to your principal balance, you can drastically reduce your loan term. This strategy accelerates your amortization schedule, meaning less of your money goes toward interest and more goes toward owning your Houston property outright.

There are two easy ways to implement this strategy:

- The Divide by 12 Method: Take your total monthly principal and interest payment, divide it by 12, and add that amount to your regular monthly payment.

- The Bi-Weekly Method: Pay half of your monthly mortgage payment every two weeks. Since there are 52 weeks in a year, you will naturally make 26 half-payments, which equals 13 full payments annually.

Before you start, always call your current loan servicer to confirm that extra funds are applied directly to the principal balance. If you want to run the numbers on your specific scenario, feel free to reach out to our team at Mpire Financial for a free consultation.

| Payment Strategy | Monthly Payment | Total Interest Paid | Years to Payoff |

|---|---|---|---|

| Standard 30-Year Loan | $1,896.00 | $382,633.00 | 30 Years |

| Bi-Weekly / Extra Payment | $1,896.00 (plus extra) | $295,120.00 | 24.5 Years |

| Total Savings | Flexible | $87,513.00 | 5.5 Years Saved |

Why This Strategy Beats Refinancing for Texas Homeowners

Refinancing makes perfect sense if interest rates have dropped significantly since you bought your home. However, if you already have a great rate on your Texas home loan, refinancing to a 15-year mortgage might force you into a higher required monthly payment. This hack gives you the best of both worlds.

By choosing the extra payment method, you remain in control. If you encounter a tough financial month, you can simply revert to your standard 30-year payment amount without penalty. As your dedicated Houston mortgage broker, I believe in strategies that empower you to build wealth safely and effectively.

Compliance & Legal Disclaimer: Jimmy Rushing, MBA | NMLS #2520082. This content is for educational purposes only and does not constitute financial advice. Loan approval is subject to credit approval and program guidelines. Contact Your Texas Home Loan Guy for personalized loan scenarios.

Q1: Can I pay off my Texas home loan early without a penalty?

Yes! Most modern conventional, FHA, and VA loans do not have prepayment penalties. However, it is always a smart idea to review your specific closing documents or contact your servicer to be completely sure.

Q2: How much does one extra mortgage payment a year save?

Depending on your interest rate and loan amount, making one extra payment per year can shave 4 to 6 years off a 30-year mortgage and save you tens of thousands of dollars in interest over the life of the loan.

Q3: Should I refinance or just pay extra on my principal?

If you want to lower your interest rate or pull cash out, refinancing is a great option. If your goal is simply to pay the loan off faster without paying closing fees, the extra principal strategy is usually the better choice.

Q4: How do I set up bi-weekly mortgage payments?

You can often set this up through your mortgage servicer’s online portal. Alternatively, you can divide your monthly payment by 12 and add that exact amount to your standard monthly payment to achieve the same result automatically.

Q5: Does paying extra principal lower my monthly payment?

No, paying extra principal will not lower your required monthly payment unless you request a loan recast. Instead, it reduces your total balance, meaning you will pay off the loan much sooner.

Ready to Optimize Your Mortgage?

Whether you want to purchase a new home, explore refinancing, or just get some expert advice, Jimmy Rushing is here to help.

Related Posts