What is a Debt Consolidation Mortgage? Are you feeling overwhelmed by high interest credit cards…

The Ultimate Guide to Refinancing Your Mortgage in 2026: Timing, Benefits, and Strategies Amid Stabilizing Rates

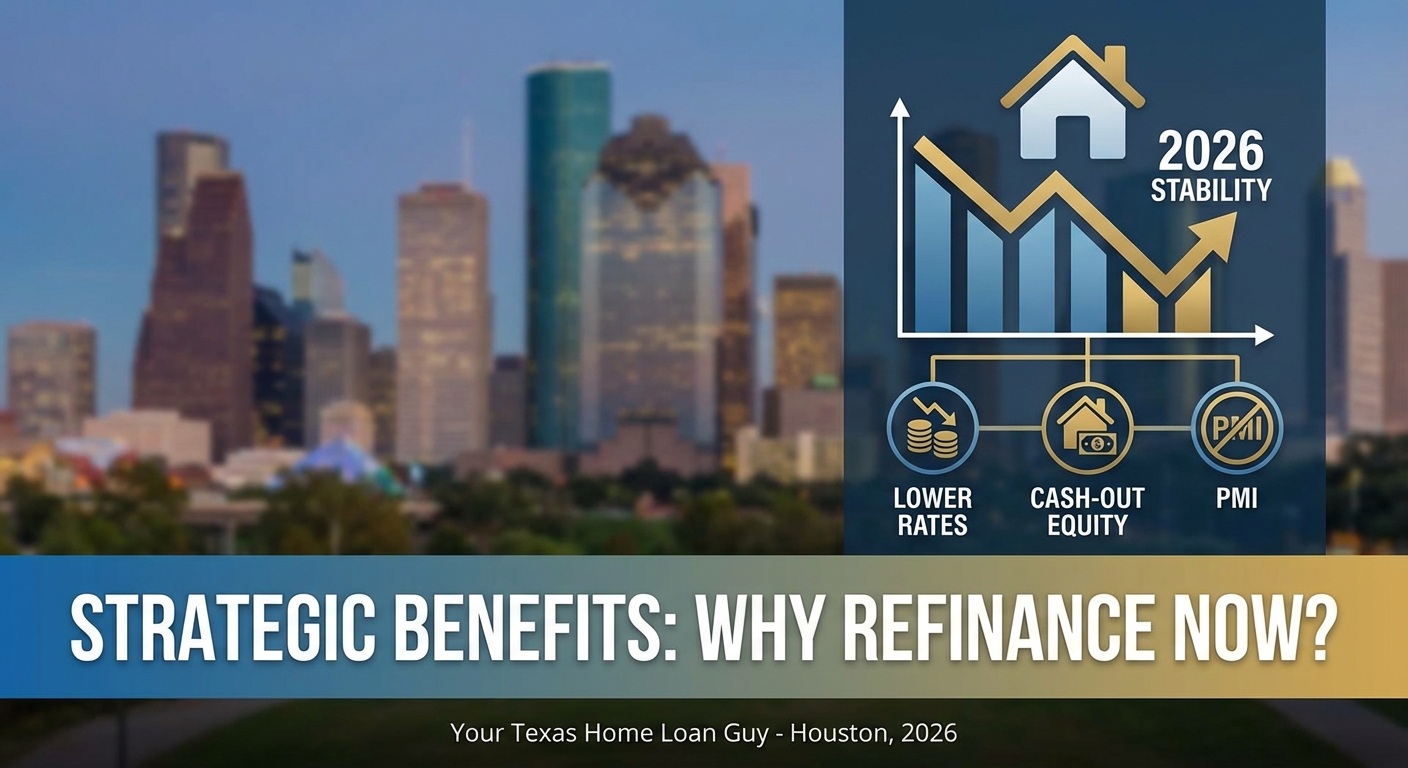

Is 2026 the Right Year to Refinance Your Houston Home?

As we settle into 2026, the real estate market is witnessing a welcome shift: stabilizing mortgage rates. After years of volatility, Houston homeowners are finding new opportunities to improve their financial health through strategic refinancing. Whether you purchased your home during the peak rate hikes or have built significant equity over the last decade, understanding the nuances of the 2026 market is crucial.

Refinancing isn’t just about securing a lower interest rate; it is a powerful tool for wealth management. At Your TEXAS Home Loan Guy, we are seeing savvy borrowers use this period of stability to consolidate high-interest debt, shorten their loan terms, or access cash for home improvements. This guide will walk you through the essential strategies to maximize your mortgage benefits this year.

Strategic Benefits: Why Refinance Now?

While a lower monthly payment is the most common motivation, the benefits of refinancing in 2026 extend far beyond cash flow. Here are the primary strategies Houstonians are leveraging:

- Rate-and-Term Refinance: This modifies your interest rate and loan term without advancing new money. If you bought when rates were hovering near 7-8%, dropping even 1% can save thousands over the life of the loan.

- Cash-Out Refinance: Texas has specific laws regarding equity (Texas Section 50(a)(6)). You can tap into your home’s equity to pay off high-interest credit cards or fund renovations, effectively consolidating debt into a tax-deductible mortgage interest payment. Reducing consumer debt often results in a significant improvement in monthly cash flow.

- Eliminating PMI: If your home value has appreciated significantly—a common trend in the Houston metro area—refinancing can help you remove Private Mortgage Insurance (PMI) if your Loan-to-Value (LTV) ratio drops below 80%.

Consulting with a local mortgage broker like Jimmy Rushing ensures you navigate Texas-specific regulations correctly.

| Scenario | Current Mortgage | Refinanced Mortgage (2026 Projection) | Monthly Savings |

|---|---|---|---|

| Loan Balance | $350,000 | $350,000 | – |

| Interest Rate | 7.5% | 6.0% | – |

| Monthly Principal & Interest | $2,447 | $2,098 | $349 |

| Total Interest (5 Years) | $128,500 | $101,200 | $27,300 (Saved) |

Calculating Your Break-Even Point

Before signing on the dotted line, it is vital to calculate your break-even point. This is the time it takes for your monthly savings to exceed the closing costs of the new loan. For example, if refinancing saves you $300 a month but costs $4,500 in closing fees, your break-even point is 15 months. If you plan to stay in your Houston home longer than that period, refinancing is a sound financial decision.

Additionally, 2026 is a prime time to review your credit score. Lenders are offering the most competitive terms to borrowers with scores above 740. If you need help understanding your credit profile or want to run specific loan scenarios, check our mortgage calculator or reach out directly to the team at Mpire Financial.

Q1: What is the ‘seasoning’ requirement for refinancing in Texas?

Generally, you must wait six months after your initial mortgage closing before you can refinance, especially for cash-out loans under Texas law.

Q2: How much equity can I access with a Texas cash-out refinance?

In Texas, you can typically borrow up to 80% of your home’s appraised value. The remaining 20% equity must remain untouched.

Q3: Will refinancing hurt my credit score?

Initially, you may see a very small dip due to the hard inquiry, but consistent payments on the new loan and reduced debt utilization usually improve your score long-term.

Q4: Are closing costs different for refinancing compared to buying?

Closing costs are generally similar, covering appraisal, title, and origination fees, but you avoid costs associated with property transfer taxes.

Q5: Can I refinance an FHA loan into a Conventional loan?

Yes! This is a great strategy to remove FHA mortgage insurance premiums once you have reached 20% equity in your home.

Ready to lower your monthly payments?

Contact Jimmy Rushing, Your TEXAS Home Loan Guy, for a Free Refinance Analysis Today!

Related Posts