Shifting Your Mindset: Why a Mortgage is a Wealth-Building Tool, Not Just Debt When most…

The Homebuyers Best Friend Playbook: What Every First-Time Buyer in Houston Should Know Before Getting Pre-Approved

Jimmy’s Educational Framework for Realistic Affordability

Stepping into the Houston real estate market as a first-time buyer can feel overwhelming. With so many neighborhoods to choose from and fluctuating interest rates, it is easy to get lost in the noise. That is where Your Texas Home Loan Guy comes in. As your dedicated mortgage broker in Houston, TX, Jimmy Rushing believes in opening doors to new possibilities through education and transparency.

One of the core pillars of our approach is understanding realistic affordability. Many first-time buyers focus solely on the maximum loan amount they can get approved for, but Jimmy’s educational framework shifts the focus to what you can comfortably afford on a monthly basis. Here is what we look at to build your confidence from day one:

- Monthly Cash Flow: Evaluating your current income against your lifestyle expenses.

- Hidden Costs: Factoring in property taxes, homeowners insurance, and maintenance.

- Future Wealth Building: Ensuring your home purchase aligns with your long-term financial goals.

By establishing a realistic budget before you even look at homes, you avoid the heartbreak of falling in love with a property that stretches your finances too thin.

Common Pitfalls to Avoid Before Your Mortgage Pre-Approval

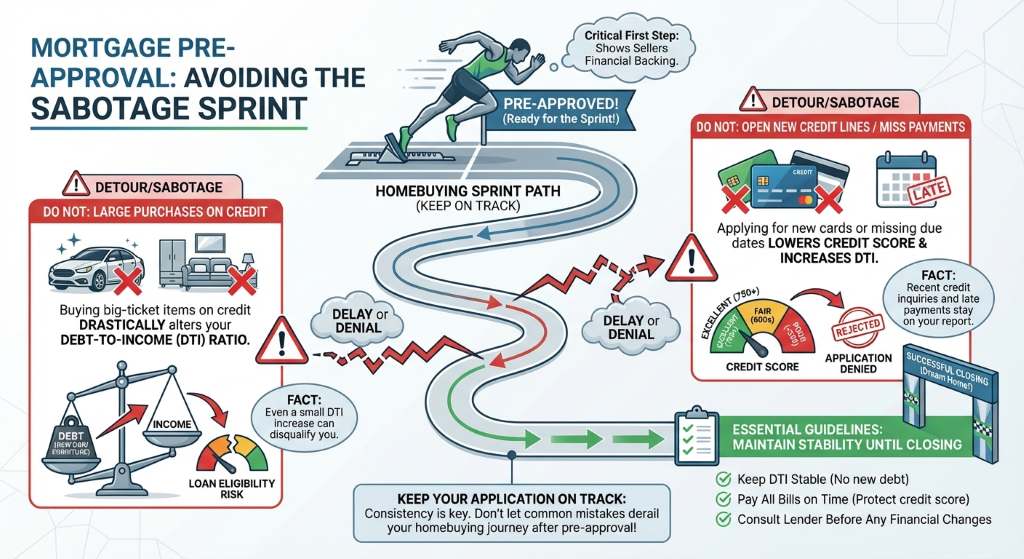

Getting pre-approved for a mortgage is the most critical step in the homebuying sprint. It shows sellers that you are a serious buyer with the financial backing to close the deal. However, many first-time buyers accidentally sabotage their pre-approval chances by making common financial mistakes.

To keep your mortgage application on track, follow these essential guidelines:

- Do not make large purchases: Buying a new car or expensive furniture on credit will alter your debt-to-income ratio.

- Do not change jobs: Lenders look for steady employment history. If you must change jobs, consult your mortgage broker first.

- Do not open or close credit accounts: Keep your credit profile exactly as it is to avoid unexpected dips in your credit score.

- Do save your documents: Keep your recent pay stubs, W-2s, and bank statements organized and easily accessible.

As your home financing partners, Jimmy Rushing and Mpire Financial will guide you through these rules to ensure a smooth, transparent, and personalized experience.

| Loan Program | Minimum Down Payment | Best For |

|---|---|---|

| Conventional Loan | 3% to 5% | Buyers with good to excellent credit scores. |

| FHA Loan | 3.5% | Buyers with lower credit scores or limited down payment funds. |

| VA Loan | 0% | Eligible Veterans, active-duty military, and surviving spouses. |

| USDA Loan | 0% | Buyers purchasing in designated rural or suburban areas. |

Building Confidence From Day One in the Houston Real Estate Market

When you partner with a local professional who is deeply invested in your success, the homebuying journey transforms from stressful to exciting. Jimmy Rushing takes pride in excellent communication and easy accessibility. Whether you are wondering about the benefits of a conventional loan or exploring Veteran Affairs financing, having an expert in your corner makes all the difference.

We offer a free, no-obligation consultation to provide personalized guidance and clarification. Our goal is not just to help you purchase real estate, but to enable you to build wealth along the way. Remember, no one will work harder on your behalf than us.

Compliance Notice: Jimmy Rushing, MBA | NMLS #2520082. Mpire Financial. All loan approvals are subject to credit and underwriting approval.

Q1: What is the difference between being pre-qualified and pre-approved?

Pre-qualification is a basic overview of your finances to estimate what you might afford. A pre-approval is a thorough review of your official financial documents, giving you a firm commitment from a lender for a specific loan amount.

Q2: How much of a down payment do I really need in Houston?

While the traditional advice is 20 percent, many first-time buyer programs allow for down payments as low as 3 percent for conventional loans, 3.5 percent for FHA loans, and even 0 percent for eligible VA or USDA loans.

Q3: Will checking my credit score for a mortgage hurt it?

When a mortgage broker pulls your credit for a pre-approval, it is considered a hard inquiry, which may cause a very small, temporary dip in your score. However, the benefit of knowing exactly where you stand far outweighs this minor impact.

Q4: How long does a mortgage pre-approval last?

Typically, a mortgage pre-approval is valid for 60 to 90 days. If you have not found a home within that timeframe, your mortgage broker can easily update your pre-approval by reviewing your most recent financial documents.

Q5: Why should I use a local Houston mortgage broker instead of a big bank?

A local mortgage broker like Jimmy Rushing has access to a diverse range of mortgage products from multiple lenders, allowing for tailored solutions. Plus, you get personalized, accessible service and deep knowledge of the local Houston market.

Related Posts