Understanding How an Adjustable Rate Mortgage Works If you are looking to buy a home…

Your Guide to Securing a Foreign National Mortgage in Houston, TX

Understanding the Foreign Buyer Mortgage Process

Purchasing real estate in the United States as a non citizen might seem like a daunting task, but securing a foreign national mortgage is highly achievable with the right guidance. Houston, TX is a booming market for international investors and prospective homeowners alike. Whether you are looking for a primary residence or exploring options for an investment property mortgage, specialized loan products are designed to meet your unique needs.

A foreign buyer mortgage provides an avenue for non US citizens to finance a home purchase. At Your Texas Home Loan Guy, we specialize in helping international clients navigate these waters. We offer tailored solutions and are experts at providing second opinions on foreign national mortgages to ensure you get the most favorable terms possible.

- ITIN Loans: Perfect for individuals who live and work in the US but do not have a Social Security Number.

- Visa Holder Loans: Designed for those legally residing in the US on temporary work visas like H1B, L1, or O1.

- Non Resident Investor Loans: Ideal for international buyers purchasing real estate purely for investment purposes.

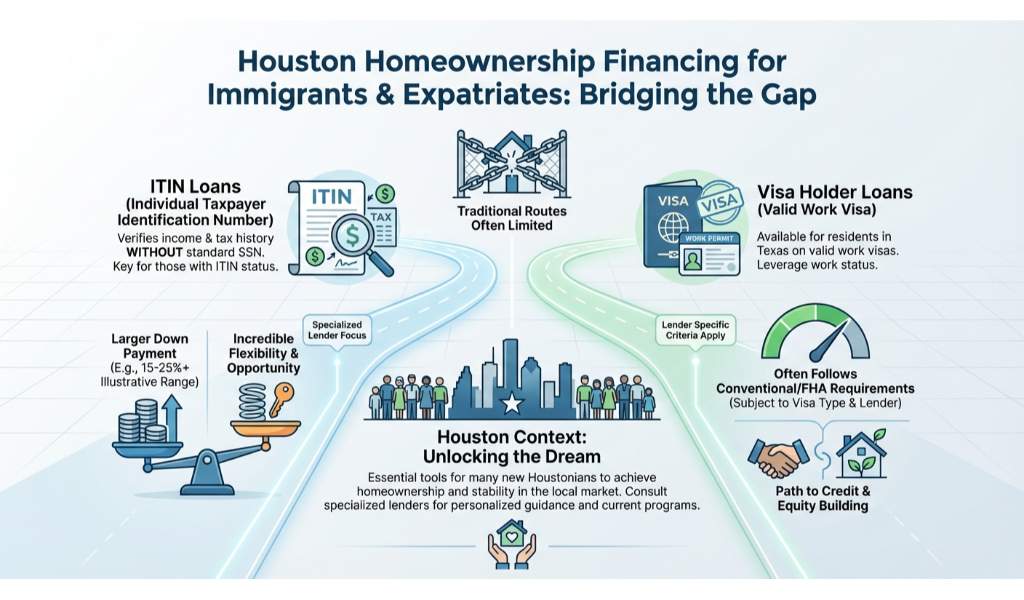

Exploring ITIN Loans and Visa Holder Loans

For many immigrants and expatriates in Houston, traditional financing routes are not an option. This is where ITIN loans and visa holder loans become essential tools for homeownership. An ITIN loan relies on your Individual Taxpayer Identification Number, allowing lenders to verify your income and tax history without requiring a standard Social Security Number. These loans often require a larger down payment but offer incredible flexibility.

If you are residing in Texas on a valid work visa, you have access to visa holder loans. Lenders will evaluate your employment stability, credit history, and visa status to approve your financing. Because homes in premium Houston neighborhoods can carry higher price tags, you might also need to explore a jumbo mortgage to fully fund your dream property.

We understand that the underwriting process for a foreign buyer mortgage can be complex. Jimmy Rushing and the team at Mpire Financial are dedicated to simplifying this process, offering clear communication and personalized guidance every step of the way.

| Loan Type | Target Borrower | Typical Down Payment | SSN Required? |

|---|---|---|---|

| ITIN Loan | US Residents with ITIN | 15% to 20% | No |

| Visa Holder Loan | H1B, L1, O1 Visa Workers | 3% to 5% (varies) | Yes (usually) |

| Foreign Investor Loan | Non Resident Buyers | 25% to 30% | No |

Why Choose Jimmy Rushing for Your Foreign National Mortgage?

Finding the right mortgage broker in Houston, TX is critical when dealing with specialized lending products. As Your Texas Home Loan Guy, Jimmy Rushing leverages deep local market knowledge and a vast network of lenders to secure the best possible foreign national mortgage for your situation. Our commitment is to educate and guide you through every step of the home financing journey.

Have you already received a quote from another lender? We are experts at providing second opinions on foreign national mortgages. Often, we can identify better rates, lower fees, or more flexible underwriting guidelines that other lenders miss. Do not leave your Texas real estate dreams to chance; work with a professional who is deeply invested in your success.

Q1: What is a foreign national mortgage?

A foreign national mortgage is a specialized home loan designed for non US citizens, including non resident investors and temporary residents, who want to purchase property in the United States.

Q2: Can I buy a house in Houston TX with an ITIN?

Yes, you can absolutely buy a home using an ITIN loan. These loans use your Individual Taxpayer Identification Number instead of a Social Security Number for income and tax verification.

Q3: What kind of down payment is required for a foreign buyer mortgage?

Down payment requirements vary by loan type. Visa holder loans might require as little as 3 to 5 percent, while ITIN loans and non resident investor loans typically require 15 to 30 percent down.

Q4: Do you provide second opinions on existing mortgage offers?

Yes, we are experts at providing second opinions on foreign national mortgages. We review your current offer and explore our network to see if we can secure better terms or lower fees for you.

Q5: Are work visa holders eligible for traditional mortgages?

Many individuals on valid work visas, such as H1B or L1, can qualify for traditional conventional or FHA loans, provided they meet specific credit, income, and residency requirements.

Related Posts