Understanding the Foreign Buyer Mortgage Process Purchasing real estate in the United States as a…

Your Complete Guide to Adjustable Rate Mortgages in Houston

Understanding How an Adjustable Rate Mortgage Works

If you are looking to buy a home in Houston, TX, you have likely come across the term adjustable rate mortgage. Also known simply as an ARM, this type of home loan offers an initial fixed interest rate for a specific period, followed by a rate that adjusts periodically based on market conditions.

Many Texas homebuyers choose an ARM because the introductory rate is often lower than what you would find with a traditional 30-year fixed-rate mortgage or a 15-year fixed-rate mortgage. This lower initial payment can help you save money in the short term, making it an excellent option if you plan to move, sell, or do a rate-and-term refinance before the introductory period ends.

ARMs come in various terms. You will often see them listed as fractions:

- 3/1 ARM and 5/1 ARM: The rate is fixed for the first three or five years, then adjusts once every year.

- 7/1 ARM and 10/1 ARM: These provide a longer initial fixed period of seven or ten years before annual adjustments begin.

- 5/6 ARM and 7/6 ARM: A newer standard where the rate is fixed for five or seven years, but then adjusts every six months instead of annually.

At Your Texas Home Loan Guy, we are experts at providing second opinions on adjustable-rate mortgages to ensure you are getting the best possible terms for your Houston property.

Navigating Caps and Floors for Your ARM

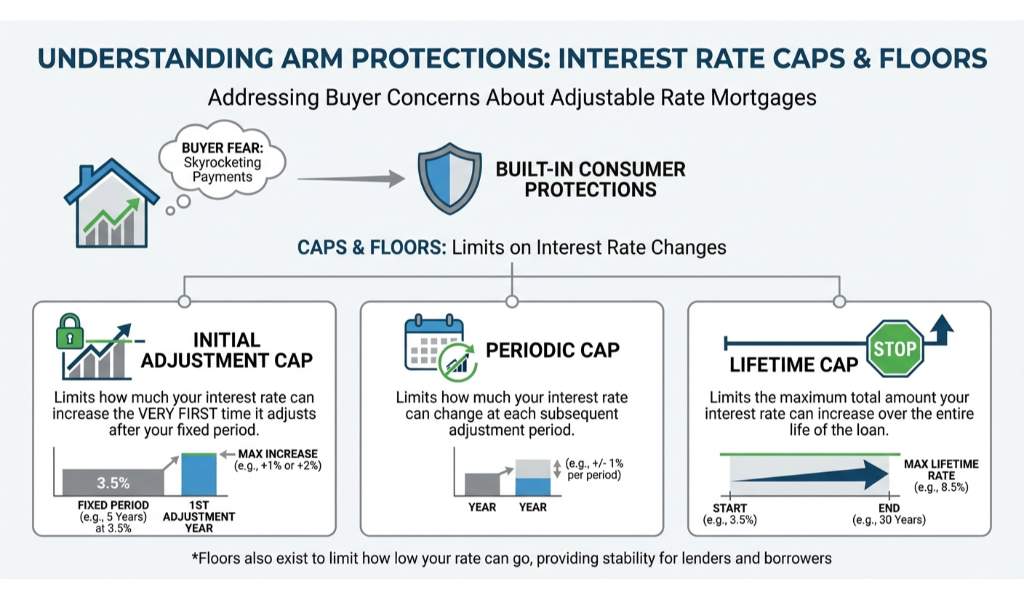

One of the biggest concerns buyers have about an adjustable rate mortgage is the fear of skyrocketing payments. Fortunately, ARMs come with built-in consumer protections known as caps and floors. These limits dictate exactly how much your interest rate can change over the life of the loan.

Here is a breakdown of the three main types of caps you need to understand:

- Initial Adjustment Cap: This limits how much your interest rate can increase the very first time it adjusts after your fixed period (like the first adjustment after five years on a 5/1 ARM).

- Subsequent Adjustment Cap: This restricts how much the rate can increase during each subsequent adjustment period (annually for a 7/1 ARM or semi-annually for a 7/6 ARM).

- Lifetime Adjustment Cap: This is the absolute maximum interest rate you will ever pay over the life of your mortgage, providing long-term peace of mind.

Conversely, a floor is the minimum interest rate your loan can drop to, even if market indices fall significantly. Whether you are looking at a standard loan or a jumbo mortgage, understanding these parameters is crucial for managing your future finances.

| ARM Type | Initial Fixed Period | Adjustment Frequency | Typical Cap Structure (Initial/Periodic/Lifetime) |

|---|---|---|---|

| 5/1 ARM | 5 Years | Every 1 Year | 2/2/5 |

| 7/1 ARM | 7 Years | Every 1 Year | 5/2/5 |

| 10/1 ARM | 10 Years | Every 1 Year | 5/2/5 |

| 5/6 ARM | 5 Years | Every 6 Months | 2/1/5 |

| 7/6 ARM | 7 Years | Every 6 Months | 5/1/5 |

Why Choose Jimmy Rushing for Your Houston Mortgage Needs

Choosing the right mortgage product is one of the most significant financial decisions you will make. As a dedicated Houston mortgage broker, Jimmy Rushing is committed to helping you navigate the complexities of the housing market. Whether you are considering a 5/1 ARM to save on early interest or want to explore a 10/1 ARM for a longer safety net, we have the local expertise to guide you.

We highly recommend getting multiple perspectives on your financing. We are experts at providing second opinions on adjustable-rate mortgages. By reviewing your current loan estimate, we can identify potential savings and ensure your rate caps align with your financial goals.

Ready to explore your options in Houston, TX? Reach out to Your Texas Home Loan Guy today to secure a competitive adjustable rate mortgage tailored to your unique needs.

Q1: What is an adjustable rate mortgage (ARM)?

An adjustable rate mortgage is a home loan that starts with a fixed interest rate for a set number of years, after which the rate adjusts periodically based on current market conditions.

Q2: How does a 5/1 ARM differ from a 5/6 ARM?

Both start with a five-year fixed-rate period. However, a 5/1 ARM adjusts once every year after the initial period, while a 5/6 ARM adjusts every six months.

Q3: Are there limits to how high my ARM rate can go?

Yes. Adjustable rate mortgages include lifetime caps, which establish the absolute highest interest rate you can be charged over the entire duration of the loan.

Q4: Is an ARM better than a 30-year fixed-rate mortgage?

It depends on your timeline. If you plan to sell your Houston home or refinance within the first five to ten years, an ARM often provides a lower initial payment compared to a 30-year fixed loan.

Q5: Can I get a second opinion on an ARM offer I already received?

Absolutely. We are experts at providing second opinions on adjustable-rate mortgages and can review your current offer to see if we can secure better terms for you.

Related Posts