Navigating First-Time Buyer Loans in Texas Buying your first home in Houston is an exciting…

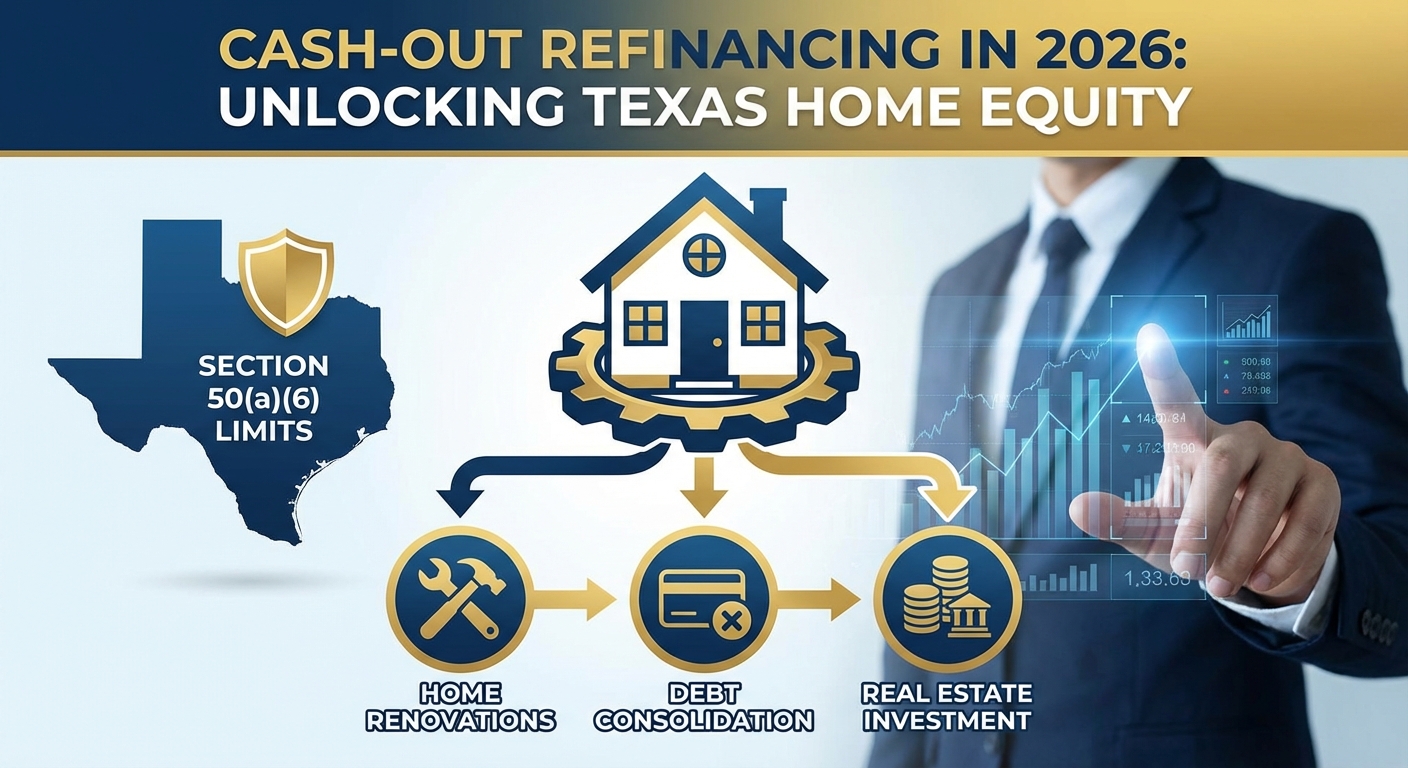

Cash-Out Refinancing in 2026: Unlocking Home Equity for Renovations, Investments, or Debt Consolidation

Why 2026 is the Prime Time to Leverage Your Texas Home Equity

As we move through 2026, homeowners in Houston, TX and across the state are sitting on record levels of home equity. Whether you purchased your home years ago or capitalized on the market shifts of the early 2020s, your property is likely your most valuable financial asset. A cash-out refinance allows you to convert a portion of that equity into liquid cash, providing a powerful tool for financial flexibility.

At Your Texas Home Loan Guy, we specialize in helping Texans navigate the unique mortgage landscape of the Lone Star State. Unlike a standard rate-and-term refinance, a cash-out refinance replaces your existing mortgage with a new, larger loan, giving you the difference in cash. This strategy is particularly effective in 2026 for homeowners looking to fund major renovations, consolidate high-interest debt, or expand their real estate portfolio.

Top Strategies: Renovations, Debt Consolidation, and Real Estate Investment

Unlocking your equity can serve multiple financial goals, but it is essential to understand how Texas laws differ from the rest of the country. Under Texas Section 50(a)(6) of the Texas Constitution, homeowners are generally limited to borrowing up to 80% of their home’s appraised value. This protective measure ensures you retain equity, but it requires strategic planning with a local expert like Jimmy Rushing.

1. Home Renovations

Reinvesting in your property is one of the smartest uses of cash-out funds. Whether you are updating a kitchen in Katy, adding a pool in Sugar Land, or fixing a roof in The Woodlands, using equity often offers a lower interest rate compared to personal loans or credit cards. Plus, these improvements can further increase your home’s value.

2. Debt Consolidation

With interest rates on credit cards and personal loans often exceeding 20%, consolidating debt into a mortgage with a much lower rate can save Houston families thousands annually. This streamlines your finances into one predictable monthly payment.

3. Investment Properties

For those looking to build generational wealth, 2026 presents opportunities to use equity as a down payment on an investment property. Leveraging your current home to buy a rental in Galveston or a fixer-upper in the loop can be a game-changer for your portfolio.

| Financial Product | Average Interest Rate (Est. 2026) | Tax Deductibility | Loan Term |

|---|---|---|---|

| Cash-Out Refinance | Lower (Mortgage Rates) | Potential (for home improvements) | 15-30 Years |

| Personal Loan | High (10% – 35%) | No | 3-5 Years |

| Credit Cards | Very High (20% – 29%+) | No | Revolving |

| HELOC | Variable (Prime + Margin) | Potential | 10-20 Years |

Navigating Texas Cash-Out Rules and Requirements

Texas is known for its unique “Texas Cash-Out” rules designed to protect homeowners. Understanding these requirements is crucial before applying. As mentioned, the Maximum Loan-to-Value (LTV) is capped at 80%. This means if your home is worth $400,000, your total new mortgage principal cannot exceed $320,000.

Additionally, there is a mandatory 12-day cooling-off period after you apply before the loan can close, and you can only execute one cash-out refinance on a property every 12 months. Credit score requirements typically start around 620, though better terms are available for scores above 740. At Your Texas Home Loan Guy, we guide you through these specific regulations to ensure a smooth closing process.

Q1: What is the maximum amount of cash I can take out in Texas?

In Texas, you can borrow up to 80% of your home’s appraised value. This total includes your existing mortgage balance plus the cash you want to take out and closing costs.

Q2: Is mortgage interest from a cash-out refinance tax-deductible?

The interest may be tax-deductible if the funds are used to buy, build, or substantially improve your home. Consult a tax professional for your specific situation.

Q3: How long does the cash-out refinance process take in Houston?

Typically, the process takes 30 to 45 days, which includes the appraisal, underwriting, and the mandatory 12-day cooling-off period required by Texas law.

Q4: Can I get a cash-out refinance with a lower credit score?

Yes, FHA and VA cash-out loans often have more flexible credit requirements than conventional loans. We can help assess your options if your score is below 640.

Q5: Are there closing costs associated with a cash-out refinance?

Yes, like any mortgage, there are closing costs (appraisal, title, origination). However, these can often be rolled into the loan amount so you don’t pay out of pocket.

Related Posts