Understanding the Emotional Rollercoaster of First-Time Homebuying Welcome to the journey of homeownership! If you…

What Credit Score Do I Need to Qualify for a Mortgage in Houston?

Buying a home is one of the most significant financial milestones in a person’s life. Whether you are eyeing a historic bungalow in the Heights, a new construction in Katy, or a spacious family home in The Woodlands, the dream of homeownership in Houston starts with one crucial number: your credit score.

As a prospective homebuyer, you likely have questions swirling around your head. Is my score high enough? Can I buy a house with bad credit? How does my credit history affect my interest rate? At Your Texas Home Loan Guy, we believe in opening doors to new possibilities, not just closing deals. We understand that your financial journey is unique, and we are here to demystify the credit requirements for securing a mortgage in the Lone Star State.

In this guide, we will break down the credit score requirements for various loan programs available in Houston, offer actionable tips to improve your standing, and explain why working with a local mortgage expert like Jimmy Rushing can make all the difference in your approval odds.

The “Magic Number”: It Depends on the Loan Program

There is no single “magic number” that guarantees a mortgage approval. Instead, the credit score you need depends heavily on the type of loan you are applying for. Different loan programs—such as Conventional, FHA, VA, and USDA—have different risk tolerances and guidelines.

While a higher score generally unlocks lower interest rates and better terms, there are plenty of options for borrowers with less-than-perfect credit. As a dedicated mortgage broker in Houston, Jimmy Rushing and the Mpire Financial team have access to a diverse range of mortgage products tailored to fit your individual situation.

Credit Score Requirements by Loan Type

To give you a clear picture of where you stand, here is a breakdown of the typical minimum credit score requirements for the most common loan programs in Texas:

| Loan Program | Typical Minimum Credit Score | Best For… |

|---|---|---|

| Conventional Loan | 620+ | Borrowers with stable income, good credit, and at least 3%–5% down payment. |

| FHA Loan | 580+ (for 3.5% down) 500-579 (for 10% down) |

First-time homebuyers, those with lower credit scores, or higher debt-to-income ratios. |

| VA Loan | No official minimum (Lenders often look for 580-620) |

Veterans, active-duty military, and surviving spouses. Offers 0% down payment options. |

| USDA Loan | 640+ | Buyers looking in designated rural or suburban areas around Houston (e.g., parts of Magnolia or Montgomery). |

| Jumbo Loan | 700-720+ | Luxury properties exceeding conforming loan limits (common in areas like Memorial, West University, and River Oaks). |

Note: While these are general guidelines, individual lenders may have “overlays” (stricter requirements). This is why working with a broker who works with multiple lenders is advantageous.

Deep Dive: Analyzing Your Loan Options

1. Conventional Loans

Conventional loans are not backed directly by the government. They are the most popular choice for Houston buyers with good credit. Generally, you need a score of at least 620. However, if your score is between 620 and 680, you might face a slightly higher interest rate or higher Private Mortgage Insurance (PMI) costs compared to someone with a score of 740+.

2. FHA Loans: The First-Time Home Buyer’s Best Friend

If you are still building your credit, or your credit score has taken a hit due to past financial struggles, an FHA loan might be your solution. Backed by the Federal Housing Administration, these loans are more forgiving.

- Score of 580+: You can qualify for maximum financing with a down payment as low as 3.5%.

- Score of 500-579: You may still qualify, but you will likely need a 10% down payment.

FHA loans are fantastic for getting into the Houston housing market sooner rather than later, allowing you to stop renting and start building equity.

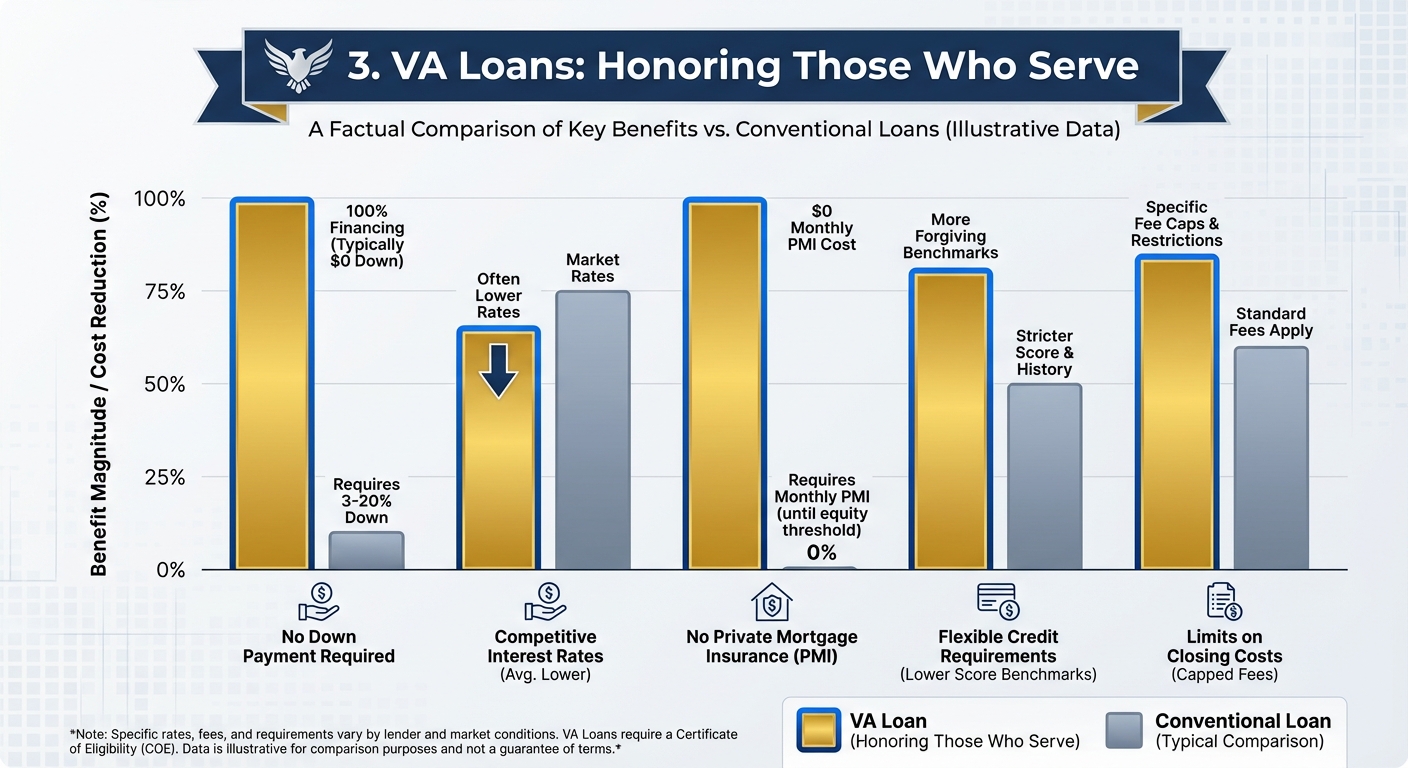

3. VA Loans: Honoring Those Who Serve

For our military community in Houston, VA loans are arguably the best mortgage product available. The Department of Veterans Affairs does not set a minimum credit score, but most lenders look for a score around 620. However, at Your Texas Home Loan Guy, we specialize in helping veterans and can often find solutions for scores lower than the industry average, provided there is a clean payment history over the last 12 months.

Why Houston Lenders Look Beyond the Score

It is important to remember that your credit score is just one piece of the puzzle. When you apply for a mortgage in Houston, lenders are looking at the “Four Cs” of underwriting:

- Credit: Your history of paying bills.

- Capacity: Your ability to repay the loan (Income vs. Debt).

- Capital: Your savings and down payment.

- Collateral: The value of the home you are buying.

Even if you have a borderline credit score, you might still qualify if you have strong “compensating factors.” These might include a larger down payment, significant cash reserves in the bank, or a low Debt-to-Income (DTI) ratio. This is where getting a personalized quote is vital—an algorithm online can’t see the full picture of your financial health, but Jimmy Rushing can.

Can I Buy a House in Houston with “Bad” Credit?

The short answer is: Yes, it is possible.

Life happens. Medical bills, divorce, or job loss can negatively impact your credit score. However, a low score doesn’t automatically disqualify you from homeownership. We work with many clients who fall into the “Fair” (600-659) or even “Poor” (< 600) ranges.

If your score is low, we don’t just say “no.” We say, “not yet, and here is the plan.” We can help you analyze your credit report to identify quick wins—such as paying down a specific credit card balance or correcting an error—that could boost your score enough to qualify. We pride ourselves on being an education-based mortgage company. We strive to provide helpful information to get you mortgage-ready.

5 Actionable Tips to Boost Your Credit Score Fast

If you are planning to buy a home in Houston in the next 3 to 6 months, take these steps now to polish your credit profile:

- Check for Errors: Pull your credit reports from the major bureaus. If you see a late payment that was actually paid on time, dispute it immediately.

- Lower Your Utilization: Credit utilization (how much of your limit you are using) is a huge factor. Try to keep credit card balances below 30% of their limit.

- Don’t Close Old Accounts: The length of your credit history matters. Keep those older credit cards open, even if you don’t use them often.

- Avoid New Debt: Do not buy a new truck or finance furniture for the new house until after you have closed on your mortgage. New inquiries can drop your score.

- Pay Everything on Time: This sounds obvious, but even one 30-day late payment can drop a good score significantly.

Pre-Qualification vs. Pre-Approval: Know the Difference

A pre-qualification is a basic estimate based on unverified information you provide. A pre-approval involves a verified review of your credit, income, and assets. In the competitive Houston real estate market, sellers want to see a pre-approval letter. It proves you are a serious buyer and that a lender has already vetted your finances.

You can start this process securely through our online application.

Why Choose a Local Houston Mortgage Broker?

You might be tempted to use a big national bank or an online-only lender. However, real estate is local. A local mortgage broker like Jimmy Rushing understands the nuances of the Texas market—from high property taxes to specific insurance requirements for coastal counties.

More importantly, as a broker, we aren’t tied to one bank’s products. We shop multiple lenders to find the best rate and terms for your specific credit profile. Whether you have a 580 score or an 800 score, we work on your behalf to structure the loan that builds your wealth.

Frequently Asked Questions (FAQs)

1. What is the lowest credit score for a home loan in Texas?

Generally, the lowest score for an FHA loan with a 10% down payment is 500, though finding lenders who participate in that program can be difficult. Most lenders prefer a minimum of 580 for FHA loans (allowing for 3.5% down) and 620 for Conventional loans.

2. Does checking my credit for a mortgage hurt my score?

A mortgage inquiry is a “hard pull” and may drop your score by a few points (typically 2-3). However, credit scoring models allow you to shop around. Multiple inquiries from mortgage lenders within a 14-to-45-day window are typically treated as a single inquiry, so don’t be afraid to get a quote.

3. Can I get a mortgage if I have a bankruptcy in my past?

Yes. For FHA and VA loans, you typically need to wait two years after a Chapter 7 bankruptcy discharge. For Conventional loans, the waiting period is usually four years. Chapter 13 bankruptcies have different, often shorter, waiting periods.

4. How does my credit score affect my interest rate?

Your credit score is a major determinant of your interest rate. A higher score signals lower risk to the lender, earning you a lower rate. On a 30-year mortgage in Houston, even a 0.5% difference in interest rate can save (or cost) you tens of thousands of dollars over the life of the loan.

5. I have no credit score at all. Can I still buy a house?

Yes, through a process called “manual underwriting.” This allows lenders to evaluate “alternative credit,” such as a history of on-time rent payments, utility bills, and insurance premiums. It is more documentation-heavy, but it is definitely a viable path to homeownership.

Ready to Check Your Eligibility?

Don’t let the fear of a credit score number keep you from your dream home. At Your Texas Home Loan Guy, we are deeply invested in your success. Whether you are ready to buy today or need a plan to get ready for next year, Jimmy Rushing and the team are here to guide you every step of the way.

Let’s see what you qualify for today!

Jimmy Rushing, MBA | NMLS #2520082

Your Texas Home Loan Guy | Mpire Financial

Phone: 713-822-6347 | Email: jimmy.rushing@yourtexashomeloanguy.com

Serving Houston, TX and the surrounding areas.

Disclaimer: The information provided in this blog post is for educational purposes only and does not constitute financial or legal advice. Loan programs, interest rates, and credit requirements are subject to change without notice. Please consult with a licensed mortgage professional for personalized guidance. Mpire Financial is an Equal Housing Lender.

Related Posts