What is an FHA Purchase Loan? If you are looking to buy a home in…

What Down Payment Assistance Programs Are Available for First-Time Home Buyers in Houston, TX?

Buying your first home is one of the most exciting milestones in life. It represents stability, community, and the start of building generational wealth. However, for many aspiring homeowners in the Greater Houston area, one significant hurdle stands in the way: the down payment.

There is a common misconception that you need a massive 20% down payment to purchase a home. In reality, that is a myth. Especially in Houston, Texas, there are numerous down payment assistance (DPA) programs designed specifically to help first-time buyers bridge the gap between their savings and the keys to their new front door.

At Your Texas Home Loan Guy, we believe that financial constraints shouldn’t keep you from achieving your dream of homeownership. As your local mortgage experts, we are here to guide you through the various grants, forgivable loans, and second lien options available right here in Harris County and across Texas.

The Challenge of the Down Payment

For many renters in Houston, the monthly mortgage payment isn’t the issue—it’s the upfront cash to close. Between the down payment and closing costs, the initial investment can feel overwhelming. This is where Down Payment Assistance (DPA) steps in.

These programs are designed to provide funds to cover some or all of your down payment and closing costs. Depending on the program, this money might be a grant (which never has to be repaid), a 0% interest loan, or a forgivable second mortgage.

Top Down Payment Assistance Programs in Houston

Houston home buyers have access to a unique mix of city-specific programs, statewide Texas initiatives, and national loan options. Below, we break down the most effective programs available to you.

1. Texas State Affordable Housing Corporation (TSAHC)

The TSAHC is one of the most popular options for Texans. They offer two primary programs that are excellent for buyers in Houston:

- Homes for Texas Heroes: Designed for teachers, police officers, firefighters, EMS personnel, and corrections officers.

- Home Sweet Texas: Designed for Texas home buyers with low and moderate incomes.

Key Benefits:

- Provides a grant or a deferred forgivable second lien for down payment assistance.

- Offers Mortgage Credit Certificates (MCC) which can provide an annual tax credit to reduce your federal income tax liability.

- You do not need to be a first-time buyer to qualify, though you must purchase the home as your primary residence.

2. Texas Department of Housing and Community Affairs (TDHCA)

The TDHCA offers the “My First Texas Home” program. This is specifically structured for first-time home buyers (defined as someone who hasn’t owned a home in the last three years).

Key Benefits:

- Offers 30-year fixed-rate mortgages with competitive interest rates.

- Provides up to 5% of the loan amount in down payment and closing cost assistance.

- Can be combined with the Texas Mortgage Credit Certificate (MCC).

3. Southeast Texas Housing Finance Corporation (SETH)

The SETH “5 Star Texas Advantage” program is another fantastic resource available to Houston residents. This program provides assistance in the form of a forgivable second lien or a grant.

Key Benefits:

- Assistance up to 5% of the total loan amount.

- No first-time homebuyer requirement.

- Income limits apply, but they are generous for the Houston metro area.

4. City of Houston Housing and Community Development Department (HCDD)

If you are looking to buy within the city limits of Houston, the local government offers substantial assistance to low-to-moderate-income families. Their program typically offers higher dollar amounts than state programs but may have stricter property location requirements.

Key Benefits:

- Historically offers up to $30,000 in assistance for qualified buyers.

- Funds can be used for down payment, closing costs, and pre-paid items.

- Requires the home to be within Houston city limits.

Note: Local government funds are often subject to availability. It is vital to speak to a local mortgage professional to check the current status of these funds.

Comparison of DPA Programs

To help you visualize your options, here is a comparison of the most common programs accessed by our clients:

| Program Name | Assistance Type | First-Time Buyer Required? | Primary Benefit |

|---|---|---|---|

| TSAHC | Grant or Forgivable Lien | No | Combines with Mortgage Credit Certificates (Tax Credits). |

| TDHCA | 2nd Lien (Repayable or Forgivable) | Yes | Competitive interest rates with up to 5% assistance. |

| SETH 5 Star | Forgivable Grant | No | Flexible income limits for the Houston area. |

| City of Houston | Forgivable Loan | Yes | High assistance amount (up to $30k) for city residents. |

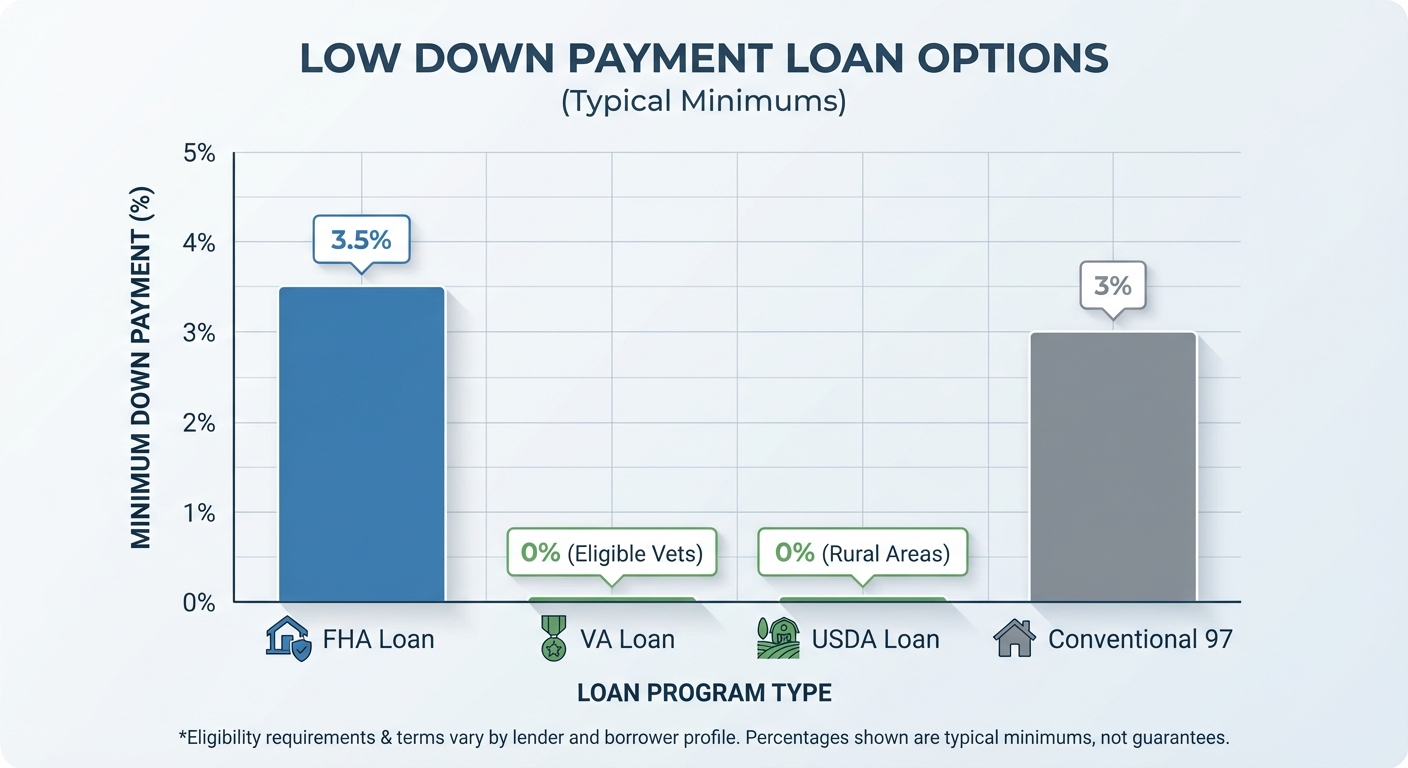

Low Down Payment Loan Options

FHA Loans

Backed by the Federal Housing Administration, FHA loans are popular among first-time buyers because they require a credit score as low as 580 and a down payment of just 3.5%. The down payment can also be fully gifted by a family member.

VA Loans

For our veterans and active-duty military personnel, the VA loan is the gold standard. It requires $0 down payment and no private mortgage insurance (PMI). If you have served, this is almost always your best option.

USDA Loans

If you are looking to buy in suburban or rural areas surrounding Houston (like parts of Montgomery or Liberty County), a USDA loan offers 100% financing (zero down payment) for qualified properties.

How to Qualify for Assistance

- Credit Score: Most programs require a minimum credit score, typically ranging from 620 to 640. If you aren’t sure where your credit stands, you can get pre-qualified to see your current status.

- Income Limits: These programs are designed for low-to-moderate-income buyers. Limits vary by county and household size.

- Homebuyer Education: Almost all DPA programs require you to complete a HUD-approved homebuyer education course. This ensures you understand the responsibilities of homeownership.

- Primary Residence: You must live in the home; these programs are not for investment properties or vacation homes.

Why Work with a Mortgage Broker?

You might be wondering, “Can I just go to my bank for this?” The answer is: maybe, but you might limit your options.

Big banks often have a limited menu of loan products. As an independent Mortgage Broker in Houston, TX, Jimmy Rushing and the team at Mpire Financial have access to dozens of lenders and specifically certified DPA programs. We shop the market on your behalf to find the specific program that fits your financial profile.

We don’t just close deals; we open doors. Our goal is to educate you, clarify the confusion, and help you build wealth through real estate.

Frequently Asked Questions (FAQs)

1. Do I have to pay back down payment assistance?

It depends on the program. Some are true grants that never need to be repaid. Others are 0% interest second loans that are forgiven after you live in the home for a certain number of years (usually 3 to 5 years). Some, however, must be repaid when you sell the home or refinance. We will help you understand the terms of each option before you sign.

2. Can I use down payment assistance with an FHA loan?

Yes! In fact, FHA loans are the most common loan type paired with down payment assistance programs due to their flexible credit requirements.

3. How long does it take to close a loan with DPA?

Using an assistance program can add a little time to the underwriting process, but not much. A standard closing takes about 30 days; a DPA loan might take 35 to 45 days. We work hard to ensure a smooth, timely closing.

4. Is down payment assistance only for first-time buyers?

First, the term “first time home buyer” is a bit misleading, as it actually refers to having not owned a home in the last three years! And on top of that, the answer is “No”! Programs like TSAHC and SETH are available to repeat buyers, provided they meet the income and credit requirements and plan to occupy the home as their primary residence.

5. What if my credit score is below 620?

If your score is below the requirement for DPA, don’t panic. We can review your credit report and offer guidance on how to improve your score. Often, small changes can boost your score enough to qualify within a few months.

Ready to Stop Renting and Start Owning?

The Houston housing market is full of opportunities, and lack of a down payment shouldn’t be the reason you stay on the sidelines. Whether you are a teacher, a veteran, or simply a hard-working Texan ready for your own space, there is likely a program to help you.

At Your TEXAS Home Loan Guy, we are deeply invested in your success. Let us run the numbers for you and show you exactly what you qualify for.

Don’t navigate this alone. Let’s find your funding today.

Get Your Free Quote & DPA Analysis

Disclaimer: Jimmy Rushing, MBA | NMLS #2520082. Mpire Financial. This material is for informational purposes only and does not constitute an offer to lend. All loans are subject to credit approval and program guidelines. Interest rates and program terms are subject to change without notice. Equal Housing Lender.

Related Posts