Navigating First-Time Buyer Loans in Texas Buying your first home in Houston is an exciting…

How Do VA Loans Work for Veterans Buying a Home in Houston, Texas?

For those who have served our country, the dream of homeownership is a well-deserved reward. If you are a Veteran, active-duty service member, or a surviving spouse looking to settle down in the vibrant city of Houston, Texas, you have access to one of the most powerful financial tools on the market: the VA Home Loan.

At Your TEXAS Home Loan Guy, we believe that understanding your benefits is the first step toward building generational wealth. Houston offers a diverse real estate market, from the bustling inner loop to the expanding suburbs of Katy, Cypress, and The Woodlands. Navigating this market requires a partner who understands both the local landscape and the intricacies of military financing.

In this comprehensive guide, we will break down exactly how VA loans work, why they are the preferred choice for Texas Veterans, and how you can leverage this benefit to buy your dream home in the Greater Houston area with $0 down.

What is a VA Loan?

A VA loan is a mortgage loan issued by private lenders—like mortgage brokers and banks—and backed by the U.S. Department of Veterans Affairs (VA). It was created in 1944 to help returning service members purchase homes without needing a down payment or excellent credit.

It is important to clarify a common misconception: The VA does not lend you the money directly. Instead, they “guarantee” a portion of the loan. This guarantee protects the lender (us) against loss if the borrower defaults. Because of this government backing, lenders can offer Veterans significantly better terms than non-veteran borrowers would receive.

The Top Benefits of Using a VA Loan in Houston

Why is the VA loan often cited as the best mortgage product available? Here are the specific advantages for Houston homebuyers:

- 0% Down Payment: This is the headline benefit. In a market like Houston, where home prices have appreciated, not having to save for a 20% down payment allows you to buy a home sooner.

- No Private Mortgage Insurance (PMI): With FHA or Conventional loans, if you put down less than 20%, you must pay monthly PMI. VA loans strictly prohibit PMI, which can save you hundreds of dollars every month.

- Competitive Interest Rates: Because the loan is government-backed, VA loans typically offer lower interest rates than conventional loans.

- Flexible Credit Requirements: We understand that military life can sometimes impact credit history. VA loans are more forgiving regarding credit scores and debt-to-income ratios.

- Limited Closing Costs: The VA limits what fees Veterans can be charged. In some cases, the seller can even pay all of your loan-related closing costs (up to 4% of the loan amount).

If you are unsure if a VA loan is right for you compared to other options, check out our guide to loan options for homebuyers.

Eligibility: Who Qualifies for a VA Loan?

To secure a VA loan in Texas, you must meet specific service requirements. Generally, you are eligible if you have served:

- 90 consecutive days of active service during wartime.

- 181 days of active service during peacetime.

- 6 years in the National Guard or Reserves.

- Or if you are the spouse of a service member who died in the line of duty or as a result of a service-related disability.

The Certificate of Eligibility (COE)

The golden ticket for your loan is the Certificate of Eligibility (COE). This document proves to the lender that you meet the military service requirements. You do not need to have this document in hand to start the conversation! As your mortgage broker, Jimmy Rushing and his team can often pull your COE instantly through our lender portal.

The Step-by-Step Process of Getting a VA Loan in Houston

Buying a home in Harris County or the surrounding areas follows a specific rhythm. Here is what the process looks like with Your TEXAS Home Loan Guy:

1. Pre-Qualification and Pre-Approval

Before you start scrolling through listings, you need to know your buying power. A pre-approval letter shows sellers you are a serious buyer with secured financing. This is crucial in the competitive Houston market.

Ready to start? Get pre-qualified securely on our website today.

2. House Hunting with a VA-Savvy Realtor

Not all homes qualify for VA financing (though most do), and not all real estate agents understand the VA contract addendum. We can connect you with local agents who are experts at negotiating for Veterans. If you need a recommendation, visit our Real Estate Agent Recommendation page.

3. The VA Appraisal

Once you are under contract, we order a VA appraisal. This is different from a home inspection. The VA appraiser does two things:

- Determines the fair market value of the home.

- Ensures the home meets the VA’s Minimum Property Requirements (MPRs)—essentially ensuring the home is safe, sanitary, and structurally sound.

Note: In Houston, common MPR issues might include roof damage or foundation issues. If these are flagged, they must be fixed before closing.

4. Underwriting and Closing

Our team works diligently to process your paperwork. Once the underwriter gives the “Clear to Close,” you will sign your documents, and the keys are yours!

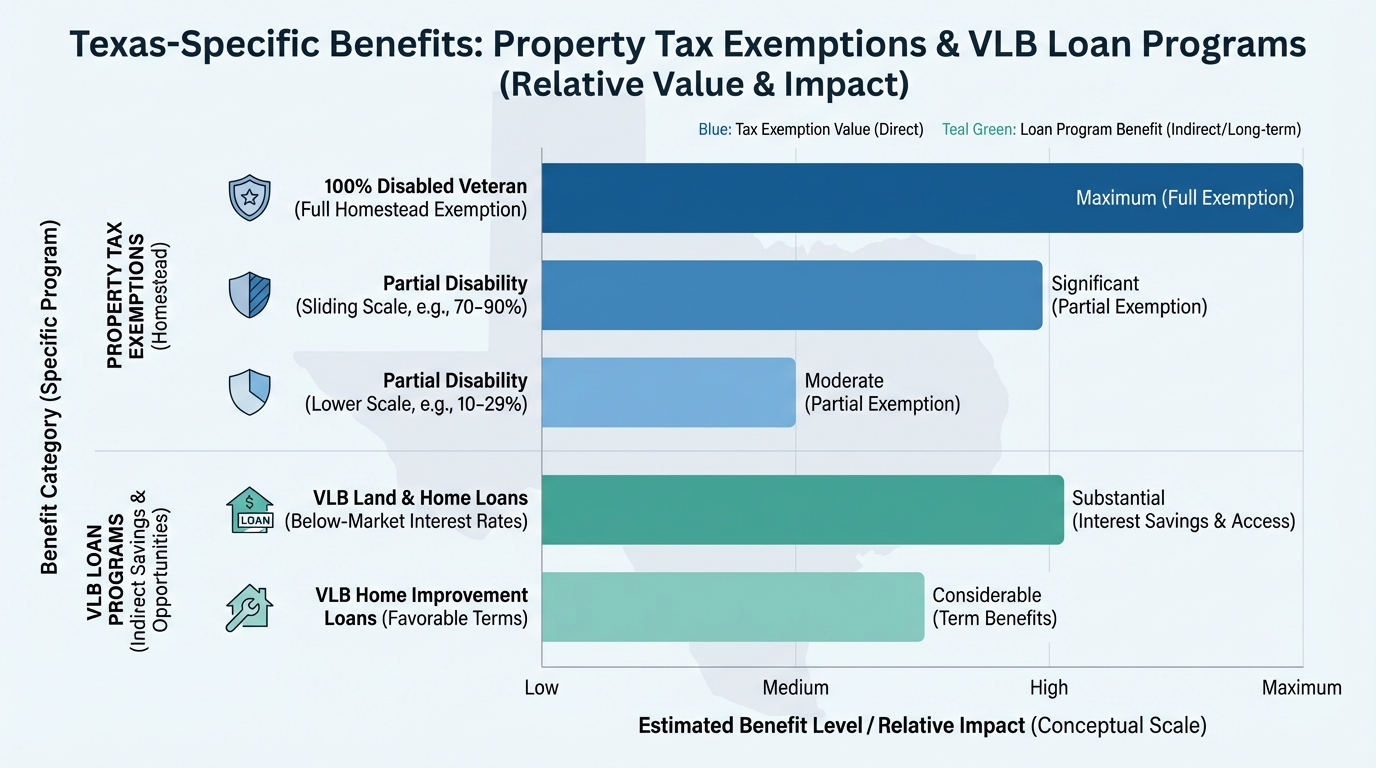

Texas-Specific Benefits: Property Taxes and the VLB

Property Tax Exemptions

Texas has some of the most generous property tax exemptions in the country for disabled Veterans. If you have a 100% service-connected disability rating from the VA, you are typically exempt from paying all property taxes on your primary residence. In Houston, where property taxes can be high, this saves you thousands of dollars annually and significantly increases your buying power.

Even with a rating between 10% and 90%, you may qualify for reductions in your home’s assessed value.

VA Loan vs. FHA vs. Conventional: A Comparison

| Feature | VA Loan | FHA Loan | Conventional Loan |

|---|---|---|---|

| Down Payment | 0% | 3.5% | 3% – 20% |

| Mortgage Insurance (PMI) | None | Required (Upfront + Monthly) | Required if under 20% down |

| Credit Score | Flexible (Often 580-620+) | Flexible (580+) | Stricter (Typically 620-640+) |

| Debt-to-Income Ratio | Highest Allowance | High Allowance | Strict Limits |

| Interest Rates | Typically Lowest | Low | Market Rates |

Understanding the VA Funding Fee

While there is no mortgage insurance, most Veterans must pay a one-time VA Funding Fee. This fee helps keep the program running for future generations. The fee ranges from 1.25% to 3.3% of the loan amount, depending on your down payment and whether this is your first time using the benefit.

Crucial Exemption: If you receive compensation for a service-connected disability (even 10%), or if you are a surviving spouse of a Veteran who died in service, you are exempt from paying the Funding Fee. This makes the loan even more affordable.

Loan Limits in Houston

Great news for 2026: There are no VA loan limits for Veterans with their full entitlement available. Whether you are buying a starter home in Pearland or a luxury estate in Memorial, lenders can finance the full amount with zero down, provided you qualify based on income and credit.

Why Choose Jimmy Rushing as Your Houston VA Lender?

Not all lenders are created equal. Big banks and national call centers often lack the specific knowledge required to close VA loans efficiently in Texas. Jimmy Rushing, “Your TEXAS Home Loan Guy” and the team at Mpire Financial take a personalized approach.

- Local Expertise: We know the Houston market, property tax rates, and local insurance requirements.

- Speed: We strive to close loans faster than the industry average.

- Education: We don’t just sell loans; we educate you on building wealth through real estate.

Visit our Learning Center for more articles on navigating the mortgage landscape.

Frequently Asked Questions (FAQs)

1. Can I use a VA loan more than once?

Yes! The VA loan is a lifetime benefit, not a one-time use. You can use it to buy a home, sell that home, and use it again. In some cases, you can even have two VA loans at the same time (called “bonus entitlement”) if you are relocating but keeping your first home as a rental.

2. Do VA loans take longer to close in Texas?

This is a myth. With an experienced mortgage broker like Jimmy Rushing, VA loans can close just as quickly as FHA or Conventional loans—often in 30 days or less. The key is working with a lender who understands the VA process.

3. Can I buy a condo in Houston with a VA loan?

Yes, but the condominium complex must be on the VA’s approved list. Houston has many approved complexes. If you find a condo you love that isn’t on the list, we can sometimes help apply for approval, though this takes extra time.

4. Is there a minimum credit score for a VA loan?

The VA itself does not set a minimum credit score, but lenders (like us) have “overlays.” Generally, a score of 620 is preferred, but we have options for lower scores depending on the full financial picture. Don’t let your credit score stop you from inquiring; contact us for a consultation.

5. Can I use a VA loan for an investment property?

VA loans are designed for primary residences only. You cannot use them to buy a dedicated rental property or vacation home. However, you can buy a multi-unit property (up to a 4-plex) as long as you live in one of the units. This is a great strategy for “house hacking.”

Ready to Use Your Benefits?

You served your country; now let us serve you. Whether you are stationed at Ellington Field, are a veteran transitioning to civilian life, or simply looking to move within Houston, Your TEXAS Home Loan Guy is here to make the process smooth and transparent.

Don’t leave your hard-earned benefits on the table. Let’s get you into a new home with $0 down and a payment you can afford.

Start Your VA Loan Application Today

Or call Jimmy Rushing directly at (713) 822-6347 to discuss your scenario.

Jimmy Rushing, MBA | NMLS #2520082 | Mpire Financial | Equal Housing Lender

The information provided in this blog post is for educational purposes only and does not constitute financial or legal advice. Loan approval is subject to borrower qualifications, including income, property evaluation, and final credit approval. Rates and terms are subject to change without notice.

Related Posts